As investors clamor for NVIDIA, a look further afield into AI plays

Asian companies with strategic AI initiatives and exposure offer buying opportunities at lower valuations to US peers despite market volatility

Over the past two weeks, we have seen an explosion in public discussion around NVIDIA Corporation ($NVDA, NVDA.US, “NVIDIA”). NVIDIA is a leading US technology company that designs and manufactures advanced graphics processing units (GPUs), and system-on-a-chip (SoC) units for the automotive and desktop / mobile computing markets. The Company has excelled in the gaming industry and in recent years has expanded its focus to include artificial intelligence (AI), autonomous vehicles, and data centers.

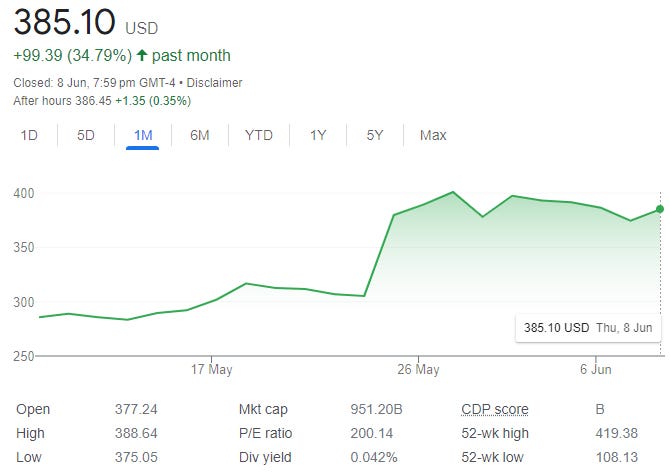

The stock has performed exceptionally well year-to-date (+170%) and flirted past the coveted USD 1 trillion market cap, joining an elite group of US tech companies such as Apple, Amazon, Google, and Microsoft, before a slight pullback.

Much of the hype came after the Company upgraded its Q2 sales guidance by 47% owing to stronger and earlier-than-foreseen AI demand. The Company’s powerful chips and data centers power AI applications and are key to building generative AI systems. NVIDIA is well covered by the market, and even with swift revenues and EPS upgrades, it appears that the sell-side has been lagging in their recognition of the Company’s potential.

Interestingly, prior to EPS upgrades, Jefferies presented a blue-skies scenario with a USD 15 EPS in 2026. The major assumptions behind it include:

• The market for data center processors will maintain a 15% CAGR.

• NVIDIA will continue to gain 500 basis points per year per share.

• NVIDIA's data center ecosystem will seize 80% of the profit opportunity in the industry from AI server expenditure

• The value of the ecosystem is comparable to that of previous computing epochs.

While NVIDIA has been performing well, the heightened discussion around the Company's growth prospects has been driven by hype around AI and the success of applications like ChatGPT. Although it is possible for NVIDIA to achieve or even exceed the average sell-side EPS consensus of USD 11 by 2026, this would require fairly optimistic assumptions.

It is important to keep in mind that the semiconductor industry, which includes NVIDIA, is known for its cyclical nature, and its demand is heavily tied to consumer demand for electronic devices. Despite NVIDIA diversifying its business lines beyond GPUs and SoCs, its valuation does seem rather untethered, which could make the stock vulnerable to market forces and external factors that could sharply drive the stock in the opposite direction.

Source: Bloomberg

Instead of pursuing growth or high valuation stocks like NVIDIA, we think there are more attractive alternatives with solid fundamentals in North Asian markets such as China, Taiwan, or South Korea. Other companies that could benefit from the growth of AI and related tailwinds include Alibaba ($BABA, 9988.HK), which we own and covered last year.

Alibaba data centers tapping into AI thematic

In our first episode, we explored how Alibaba's Middle East growth is being driven by its cloud computing and AI services arm, Alibaba Cloud. We discussed the potential opportunities emerging in the region, thanks to the advanced capabilities of Alibaba's AI data center services. Now, we provide an overview of the Company’s strategic direction and latest developments in sizing it up as an investment opportunity.

Alibaba's cloud unit, also known as Cloud Intelligence Group, is the leading cloud provider in China (36% market share and 7% yoy growth in 2022) and one of the largest in the world. Alibaba’s cloud revenue declined by 2% yoy to CNY 18.6bn due to delayed hybrid cloud projects and decreased content delivery network (CDN) demand. However, recent discounting should help Alibaba scale its business and generative AI should spur increased demand for computing power and new applications.

Major restructuring plan to boost competitiveness and streamline decision making

In March 2023, Alibaba announced a major restructuring plan that will split its business into six independent units: cloud, e-commerce, local services, logistics, global digital business, and digital media & entertainment. The Company said this move will help each unit become more agile, competitive and responsive to market changes. It will also allow them to raise funds and go public separately, except for the e-commerce unit, which will remain wholly owned by Alibaba. The plan was well received by investors, who pushed Alibaba's shares up by more than 14% in the US on the day of the announcement. Alibaba's board has approved a reorganization plan that includes:

1) Cloud Intelligence Group spin-off via stock dividend distribution to shareholders;

2) Seek external capital raising for international e-commerce operation;

3) Cainiao IPO (Alibaba logistics arm); and

4) Freshippo IPO (Alibaba grocery arm).

The Company aims to complete these initiatives within 6-18 months.

Alibaba's focus will shift towards capital management and boosting shareholder returns. While Taobao & Tmall Group will remain entirely owned by Alibaba Group, each of the other units will have the flexibility to pursue IPOs and raise external capital.

New strategic initiatives for the next 3-5 years

Alibaba is restructuring its operations to empower each business unit to develop its 3-5-year strategy for sustainable growth. The Cloud Intelligence Group is reducing prices to expand its customer base and focusing on cloud services. AliCloud is launching a chatbot for use across its apps and services and preparing for an IPO to raise funds from external investors. The Company plans to distribute shares of its cloud unit as stock dividends to its shareholders.

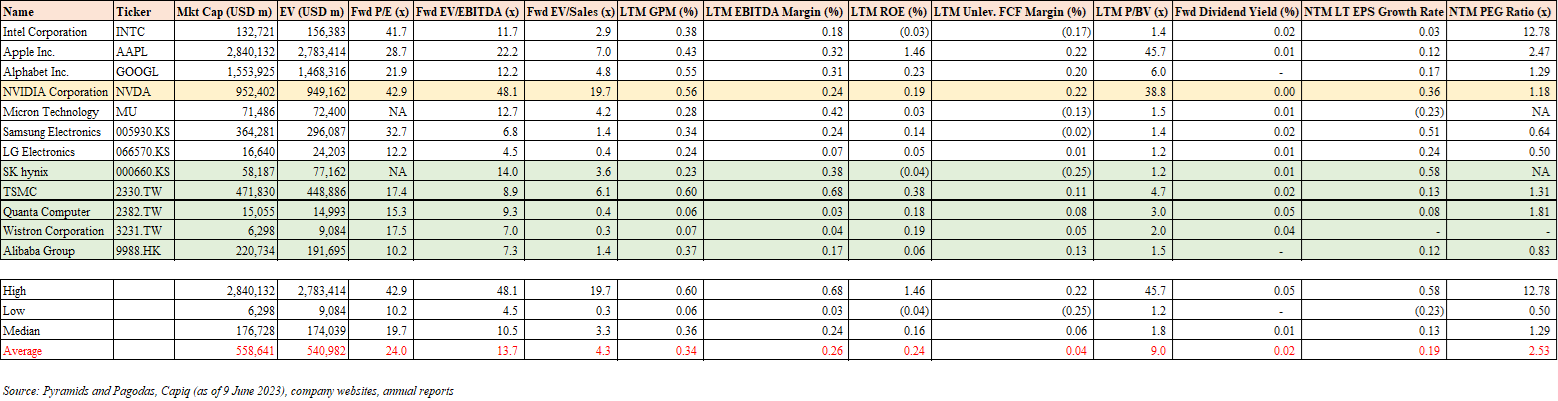

The stock is trading at a forward P/E, EV/EBITDA and EV/Sales of 10x, 7x and 1.4x respectively.

Further opportunities in the semiconductor space from Taiwan

In addition to Alibaba, some other names that could benefit from the NVIDIA and AI thematic include, but are not limited to Quanta Computer (2382.TW), Taiwan Semiconductor Manufacturing Co. (2330.TW, “TSMC”), and Wistron Corporation (3231.TW).

Quanta and Wistron are both Taiwanese original design manufacturers (ODM) that provide design, manufacturing, and after-sales services for a wide range of electronic products, including smartphones, notebooks, servers, and storage devices. Both names offer indirect exposure to AI-related growth as their customer base includes the likes of Apple, Amazon, Google, Hewlett Packard, Microsoft, and NVIDIA, all of which are heavily invested in the thematic.

Quanta is at the tail end of inventory adjustments (on general servers) and expects to see sales recover in Q223e. Despite an anticipated decrease of around 5% yoy in 2023e sales, Quanta’s server business, particularly its cloud/AI servers and automotive (EV/vehicle computing and advanced driver assistance systems products) segments are key catalysts for growth over the next two years:

• Server sales are expected to grow by single and double digits respectively in 2023e and 2024e, driven by sales of high-ASP AI servers (3x ASP of normal servers) in H223e, which could offset slower growth in its general servers segment.

• The automotive segment’s contribution to sales is expected to increase from high single-digit to low double-digit from 2023e to 2024e from landing Tier 1 EU and US clients.

• Notebook/laptop sales weighting is projected to fall below 45%, which would be positive for its gross margins.

Management is guiding for stable operating margins in 2023e, while consensus is that the Company can achieve margin expansion and sales growth in the coming years driven by the aforementioned cloud server and automotive verticals. The stock is trading at a forward P/E and EV/EBITDA of 15x and 9x, respectively, with a 5% forward dividend yield.

Wistron reported lower-than-expected Q123 EPS due to higher non-operating loss, but anticipates improved gross and operating margins in 2023e. The server business is expected to drive growth, due to the Company winning orders related to AI servers from the likes of Cisco, Dell, and NVIDIA. Wistron also foresees stronger sales from GPU accelerator projects, offsetting falling sales from Wiwynn, a Wistron subsidiary specializing in cloud infrastructure solutions. Analyst consensus is that Wistron’s focus on operating margin expansion in 2023-24e should deliver 30% earnings growth by 2024e. The stock currently trades at 17x and 7x forward P/E and EV/EBITDA, respectively, with a 4% forward dividend yield.

Taiwan Semiconductor Manufacturing Company (TSMC) is a leading semiconductor foundry with expertise in advanced chipmaking, including AI and related technologies. As a critical player in the global tech supply chain, the Company is widely exposed to different end applications, making it a proxy for the global tech demand outlook. Although TSMC’s revenues are forecasted to decline by around 4% in 2023e, inventory corrections and computing demand from 5G, AI, and networking contribute towards strong revenue and earnings growth momentum into 2024e and 2025e. Furthermore, the Company’s expanding industry leadership, strong capex cycle, and increasing demand for automotive chips are among the factors that should help to drive TSMC's valuation higher as we enter the recovery phase of a bottoming out tech demand downcycle. The stock is trading at a forward P/E and EV/EBITDA of 17x and 9x respectively, with a 2% forward dividend yield.

South Korea-based manufacturers also cashing in on AI trend

We also think South Korea’s SK Hynix (000660.KS), a global supplier of dynamic random-access memory (DRAM) chips and flash memory chips, as an attractive trade. The Company is the second-largest memory chipmaker and third-largest semiconductor player globally. The memory market outlook is showing signs of improvement, with a projected turning point moving into H223e due to declines in supplier and customer inventory levels. SK Hynix is looking to hike prices, particularly on products targeting the AI server market like its DDR5 SDRAM, which is seeing strong demand and tight supply. The Company’s earnings are expected to stabilize despite the short-term absence of a significant uptick in client demand.

We expect the increasing demand for high-capacity products, supply cutbacks, and inventory adjustments, coupled with the AI deployment to lead to consensus EPS upgrades on the stock. The reduction in cyclicality should also spur a gradual multiple re-rating for SK Hynix. Despite the recent share price rebound, the stock is still only trading at a price to book (P/B) ratio of 1.2x, which is within and at the lower end of the 1x-2.5x range over the cycle.

Summarizing the alternative investment opportunities to NVIDIA

Each of upstream names mentioned above are well positioned to capture the AI and machine learning (ML) transition over the next two years, while addressing inventory problems in face of weak consumer demand globally. These are positive factors for stock re-ratings in the coming 12-18 months.

Stock - 1M performance

BABA +5.73%

TSMC +12.33%

Quanta +43.40%

Wistron +51.77%

SK Hynix +31.88%

NVIDIA +34.79%

While most of the cycle-bottom trades have occurred (the easy money has been made), companies must now demonstrate a sustainable demand recovery to justify higher valuations. At the same time, the relatively richer multiples would suggest that the buy-side is expecting a revenue and earnings snapback in H223e and 2024e. It wouldn’t be out of the question to see the broader tech sector experience a sales rebound as supply chain bottlenecks are removed.

Source: Pyramids and Pagodas, Company data, Yahoo Finance

We like the opportunities here in Asia as they are significantly cheaper than US counterparts, as has been the case historically. We foresee buying opportunities in the coming quarters as markets remain volatile.

Currently, we are long Alibaba and establishing trading positions in TSMC and SK Hynix as opportunistic North Asian plays at a pivotal moment in the cyclical low and beneficiaries of strong AI/ML demand and deployment.

Disclaimer: This research piece above is for informational, entertainment, educational, and/or study or research purposes only. The information contained herein or discussed does not, should not, and cannot be construed as or relied upon and, for all intents and purposes, does not constitute or provide professional financial, investment, or any other form of advice. This research does not and should not be construed as an offer to sell or the solicitation of an offer to buy any securities or any other financial instruments in any jurisdiction, including where such actions are illegal. This research is not intended for publication in jurisdictions where it would violate laws. The research does not consider individual investment objectives or financial positions and merely expresses the opinions of its authors. Any investment involves taking substantial risks, including (but not limited to) the complete loss of capital. Every investor has different strategies, risk tolerances, and time frames. You are advised to perform your own independent checks, research, or study, and you should consult a licensed professional before making any investment decisions. The assumptions and parameters discussed or used are not the only reasonable ones, and no guarantee is given for their accuracy, completeness, or reasonableness. No promise is made that any indicative performance return will be achieved. The research is derived from public information sourced by Pyramids and Pagodas. No representation or warranty is given for the reliability, completeness, timeliness, accuracy, or fitness of this research, nor is any responsibility or liability accepted for any loss or damage. The authors (Pyramids and Pagodas) shall in no event be held liable to any party for any direct, indirect, punitive, special, incidental, or consequential damages arising directly or indirectly from the use of any of this material.