On 2 November 2022, People’s Daily Arabic ran a piece highlighting the role of Chinese companies in the rapid expansion of renewable energy capacity in Egypt. This is topical at the moment, given Egypt recently hosted the COP27 summit in Sharm el-Sheikh (from 7-18 November) and is keen to brandish its recent progress in renewable energy to the world. The companies mentioned in People’s Daily article included TBEA Co. Ltd. (600089.SS, “TBEA”) and Zhejiang CHINT Electrics Co. Ltd (601877.SS, “CHINT”). China Jushi Co Ltd. (600176.SH) also caught our attention given its large and growing fiberglass manufacturing presence in the country. A significant proportion of the growing demand for fiberglass is being driven by renewable energy generation – a trend that will only accelerate both in Egypt and globally. In this article, we provide some background on Egypt’s renewable energy drive and the role of Chinese companies in this, and a high-level look into Jushi’s fundamentals with a view to take a small position as a renewables and China re-opening play.

Source: COP27

Blessed by sunny skies and windy shores – Is Egypt an emerging renewables powerhouse?

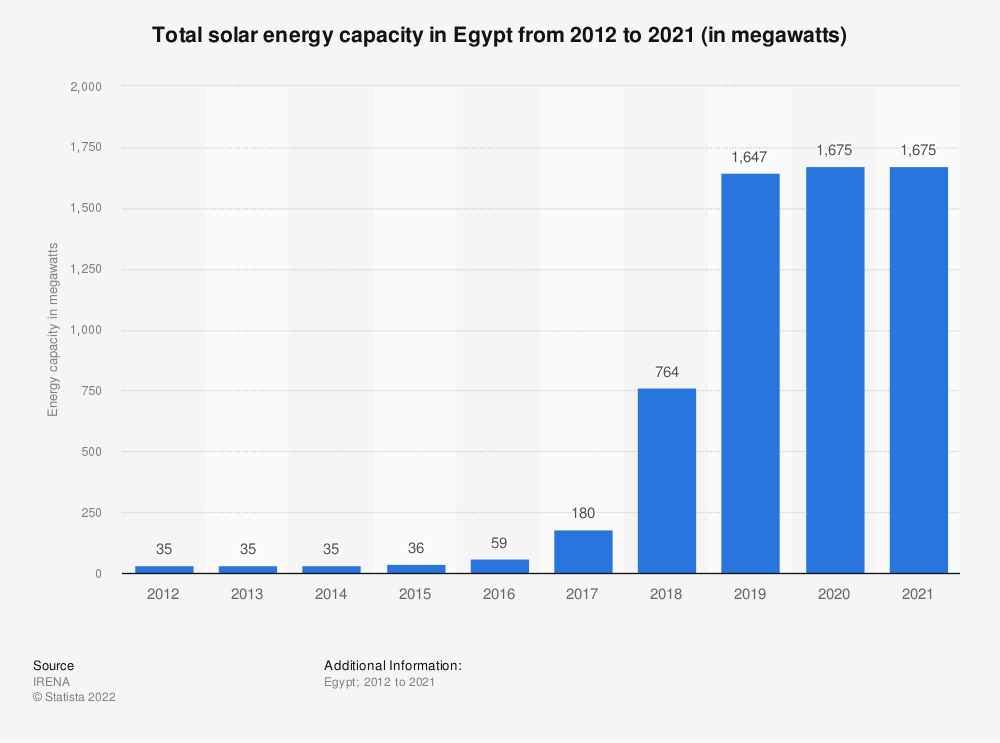

First and foremost, Egypt has excellent potential for renewable energy, with high solar irradiation, windy coasts, and abundant state-owned and uninhabited desert land. In 2012, the country set ambitious targets for renewable energy at 20% of total electricity generation by 2020. Despite this figure only reaching 12% in 2020, it doesn’t tell the full story. A significant improvement in the security situation post-2016 and more investment-friendly policies being rolled out have led to a significant acceleration in growth in the past four years. The stalling growth in wind power is somewhat misleading, as market research indicates that around 1000 MW of capacity is coming online in the next two years alone. In general, the government’s focus on renewables is more about economics than the environment – much of Egypt’s rapidly growing energy demand is being fed by natural gas, which of course Cairo would rather export in today’s pricing environment.

Source: Statista

Much of the growth in renewable energy generation is led by large-scale public sector projects. A big question asked by analysts is why installations of rooftop solar have not seen similar growth. Consumers are still put off by high upfront costs, but this too looks like it will change as the government rolls out supportive financial policies and cuts red tape, costs of grid electricity increase (due to fossil fuels costs), and solar panel prices fall. These factors are also boosting the financial viability of large-scale private and public sector projects, and many of these benefit from cheap credit from Chinese commercial and western development banks. New factories and industrial parks focusing on the domestic production of solar panels are in the works. According to an August 2022 Bloomberg Asharq report, unspecified Chinese companies are in talks with the Egyptian government to set up a USD 2.3 billion solar panel manufacturing cluster.

Benban Solar Park in Aswan, Egypt (Source: Egypt Independent)

The most prominent of the generation projects was the recently completed 1650 MW Benban Solar Park in Aswan, which is the fourth largest in the world. The project, which created 3,000 local jobs, used panels supplied by TBEA. CHINT was involved in the park’s construction, while Chinese state-owned bank ICBC (1398.HK) provided financing.

Fiberglass manufacturers to benefit from local and global push for renewables

China Jushi Co Ltd. (600176.SH, “Jushi”, “the Company”), established in 1993 and listed in the China A-share market, is a Chinese fiberglass manufacturer with a significant and growing presence in Egypt. For starters, fiberglass is a widely used material in automotive and aircraft manufacturing, construction, and telecoms equipment, among others. It can serve as replacement for traditional materials including wood, steel and even cement. Its end-use applications include insulation, reinforcement in plastics, industrial filtration, belting, type cords, and textiles.

Increasingly, growth in fiberglass demand is being driven by renewable energy demand, particularly from wind power generation. The global fiberglass market was estimated at USD 27.1 billion in 2021, and by some conservative estimates could reach USD 35.69 billion in 2028. Interestingly the growth of renewable energy output in Egypt is estimated at 10-15% for the next decade, with similar growth forecast in other major regional markets such as Saudi Arabia, the UAE, Morocco, and South Africa. This could be an interesting positioning for Jushi as several of these countries are attempting to onshore parts of the renewable energy and electric vehicle supply chain. Jushi offshoring a portion of production also provides some relief from COVID-19 restrictions back home, as well as increasingly hostile trade policies targeting Chinese exports.

The fiberglass manufacturing sector is one of the brighter spots we see in Egypt’s economic prospects moving ahead. As we highlighted in our previous macroeconomic overview podcast on Egypt, the country has a competitive advantage in energy-intensive industries such as petrochemicals, steelmaking, ceramics, and of course fiberglass due to its relatively low energy costs and abundant natural gas reserves. The country also has extensive reserves of high-quality sand, which the whole glass industry benefits from. Egypt is now the third largest fiberglass producer in the world, with Jushi being the dominant producer in Egypt. 99% of Jushi’s output in Egypt (200,000 tons) is exported, according to the Company.

Inside One of Jushi’s Factories (Source: CGTN)

Jushi’s fiberglass factories in Egypt are already some of the largest in the world, and in August 2021 the Company announced it would spend USD 335 million to expand capacity in Egypt by another 120,000 tons to be ready in early 2023. Interestingly, this announcement came after the Company stated it had cancelled plans to build similar capacity in India (a key export market for Egyptian fiberglass) due to COVID-19. Jushi’s factories in China and Egypt will now supply the Indian market. While potential trade risks are apparent with the EU and US slapping tariffs on Egyptian and Chinese fiberglass exporters, much of the export is likely destined for other key growth markets like Saudi Arabia and India and local demand is likely to grow significantly as discussed above.

Jushi Egypt (Source: Youm7)

A glance at Jushi’s fundamentals

Jushi is a vertically integrated fiberglass pure play with prominent scale and cost leadership. In China, the Company accounts for over 30% of total output in an oligopolistic market 80% controlled by the top five players. Globally, Jushi holds 20-25% market share with a presence across five continents. The domestic market has been a key source of growth for Jushi owing to technology upgrades and new tank furnace capacity construction over the past 10 years. Since 2010, the Company has scaled revenues at an 11-year CAGR of 13.8% to CNY 19.7 billion (USD 2.83 billion), with domestic business accounting for 64% of sales and the remainder being derived from overseas. The Company’s production capacity has more than tripled to over 2 million tons of fiberglass yarn. Jushi’s net-profit-after-tax (NPAT) increased 20-fold to CNY 6.03 billion (USD 867 million) and it has consistently delivered an above 28% payout to shareholders (currently at 3.3% dividend yield).

Jushi Domestic Market Share Estimates (Source: J.P. Morgan)

The fiberglass industry is cyclical in nature, particularly for building materials. Domestically, the market hit a downturn post-2008, but subsequent policy stimulus in infrastructure, renewable energy, and auto manufacturing paved the way for new growth. The sector peaked again in 2018-19 after seeing nearly 900k tonnes of capacity added, which created a supply and demand imbalance, driving roving prices downwards. However, diversity in fiberglass products and applications can smooth out fluctuations in certain segments. As is the case for Jushi, which diversified its fiberglass products portfolio in the peak upcycle of 2020-21. More recently, the industry has been exhausted by oversupply and the lasting effects of the trade war and COVID-19 lockdowns, which led to historical lows for fiberglass prices. Analysts expect sector profits to bottom out in Q422. Small-to-medium enterprises are very likely to be unprofitable due to higher input costs and lower sales prices.

Despite these challenges, Jushi continues to maintain its competitive edge owing to significantly lower production cost per tonne relative to peers and strong loyal downstream customers. In Q322, Jushi showed a much slower revenue decline than sector average, while strong cost-control (cost per unit of production output) are enabling more upside surprises. Margins and return on equity (ROE) have increasingly seen improvements. Management believes that recent concerns around pricing pressures are overblown and can be absorbed by growing demand from wind, auto, and printed circuit boards (PCBs), which account for 40%, 40%, and 20% of the Company’s revenues, respectively.

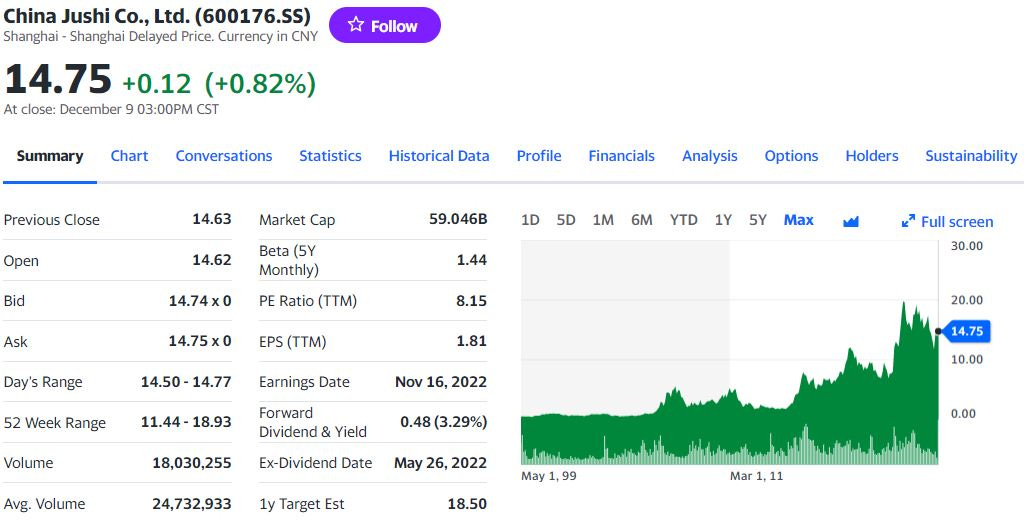

Stock performance has recovered 12% over the past month, but remains muted after declining -19% year-to-date. Jushi is trading at a forward P/E and P/BV of 7.2x and 1.8x, which represents a ~60% discount to its 5-year forward P/E median and a 0.5 standard deviation below its historical P/BV average. However, a shorter term view is that current stock price trading range is fair having come out of a peak 2020-21 upcycle. As at 9 December 2022 close, Jushi’s market cap is around CNY 59.0 billion (USD 8.5 billion); total cash and debt on balance sheet is approximately CNY 4.3 billion (USD 0.6 billion) and CNY 13.2 billion (USD 1.9 billion) respectively.

Source: Yahoo Finance

That said, we like taking a small stab at Jushi here. Planned expansions in China and abroad will add a further 30% to capacity in 2022-23. This figure represents 32% of production capacity added by Chinese fiberglass players between 2021 and 2023. We do see oversupply as a short-term headwind, but Jushi should in any case be able to weather the storm. The Company’s significant scale should allow for it to further capture and/or retain its global market share despite the challenging operating environment. The demand for EVs, appliances, energy conservation products, and renewables will be driving catalysts for the stock over the next several years. We think Jushi at current levels is an attractive enough proposition to play at these longer-term thematics as supply-demand dynamics self-correct.

There are several tailwinds for Jushi that should help manifest an improvement in stock performance. Domestically, the easing of China’s zero-COVID policy and continued infrastructure and renewables expansion are the main demand drivers for fiberglass and subsequent yarn price hikes. Jushi will benefit from a ramp-up in large wind and solar projects both in China and overseas. There could also be increased interest for Chinese fiberglass considering supply chain disruptions and with high gas prices unlikely to budge in Europe.

Full disclosure: Both me @TheAltraman and @Desertfox currently own the stock.

Disclaimer: This research piece above is for informational, entertainment, educational, and/or study or research purposes only. The information contained herein or discussed does not, should not, and cannot be construed as or relied upon and, for all intents and purposes, does not constitute or provide professional financial, investment, or any other form of advice. This research does not and should not be construed as an offer to sell or the solicitation of an offer to buy any securities or any other financial instruments in any jurisdiction, including where such actions are illegal. This research is not intended for publication in jurisdictions where it would violate laws. The research does not consider individual investment objectives or financial positions and merely expresses the opinions of its authors. Any investment involves taking substantial risks, including (but not limited to) the complete loss of capital. Every investor has different strategies, risk tolerances, and time frames. You are advised to perform your own independent checks, research, or study, and you should consult a licensed professional before making any investment decisions. The assumptions and parameters discussed or used are not the only reasonable ones, and no guarantee is given for their accuracy, completeness, or reasonableness. No promise is made that any indicative performance return will be achieved. The research is derived from public information sourced by Pyramids and Pagodas. No representation or warranty is given for the reliability, completeness, timeliness, accuracy, or fitness of this research, nor is any responsibility or liability accepted for any loss or damage. The authors (Pyramids and Pagodas) shall in no event be held liable to any party for any direct, indirect, punitive, special, incidental, or consequential damages arising directly or indirectly from the use of any of this material.

References:

https://www.fortunebusinessinsights.com/fiberglass-market-102338

http://www.xinhuanet.com/english/2018-01/10/c_136883607.htm

http://arabic.peopledaily.com.cn/n3/2022/1102/c31660-10166484.html

https://www.asharqbusiness.com/article/41151

https://news.cgtn.com/news/33677a4d7a677a6333566d54/share_p.html

https://egyptianstreets.com/2015/12/04/egypt-launches-the-largest-wind-farm-in-africa/