Overview and takeaways on Chinese commercial activity in the Middle East and beyond #4

1 Apr - 30 Apr 2022

CONTENTS

1) Saudi Arabia Reduces 36.7% of its Holdings of US Treasury Securities in Two Years

2) Sino-Iranian Relationship Trumpeted While Implementation Remains Lacking and Beijing Eyes Lucrative Gulf Ties

3) Chinese Investments in Algerian Phosphate as a Means to Reduce Dependence on Morocco?

4) China’s Oil Champion CNOOC Resumes Normal Operation of its Overseas Assets in Canada, Britain, and the US While Focusing on Friendlier Neighborhoods

1) Saudi Arabia Reduces 36.7% of its Holdings of US Treasury Securities in Two Years

Financial news outlet Zawya reported on 20 April 2022 that Saudi Arabia had reduced 36.7% of its US treasury securities over two years as of February 2022. Right on cue, in fact, highlighted in our first newsletter in early February the Kingdom’s debt dump in 2021, which has only accelerated since the Russia-Ukraine conflict.

The article cited an economic analyst Dr. Salem Bajaja, who seemingly brushed off Saudi Arabia’s dump as a re-balancing exercise and used examples of Brazil, Ireland, Luxembourg, and Hong Kong, which also reduced holdings during the COVID-19 era to support this narrative.

Buying and selling US treasury securities and other investment means are usually subject to periodic evaluation. Similar is the case with their feasibility compared to other types of investments, in addition to the need for some countries to monetize their investments when needed.

With respect to Dr. Bajaja, we think he has missed the forest for the trees. There is an entire geopolitical backdrop that is missing from his view. We believe that Saudi Arabia’s active re-balancing from US treasuries is a long-term strategic play especially taking into context of the following:

1) The weaponization of FX reserves (subject to seizures or freezes by the US and EU), which we have covered extensively in our Impact of Sanctions on Russia Fades Amid Shifting Sands of New World Order? piece.

2) USD hegemony when dealing with internal affairs, and benefits for Saudi diversification of dollar investments, which we covered in our Saudi Arabia in Talks to Price Oil Exports to China in Yuan Instead of USD piece.

3) Significant strains on US-Saudi relations. The White House has previously requested the Saudis to pump more oil to tame prices and undercut Moscow’s war chest, but the Kingdom has kept in line with Russian interests and very much aligned itself with the Eurasian bloc (including its biggest partner China).

We have seen seizure and freezing of assets by the West throughout history, but critically not targeting a G20 (nuclear-armed) nation. Many nations may potentially be considered as bad actors by the West depending on circumstances, including Saudi Arabia (given the Jamal Khashoggi and Yemen situations). The ability to discredit one sovereign savings incentivizes diversification, which we think is part of the Kingdom’s agenda now. What we are witnessing is the nature of realpolitik, whereby to safeguard a nation’s assets, accrued economic surpluses are not going to be put into place where they can be used against you, especially as tensions rises globally.

References:

https://www.zawya.com/en/wealth/wealth-management/saudi-arabia-reduces-367-of-its-holdings-of-us-treasury-securities-in-two-years-utu3efvn

https://www.wsj.com/articles/how-u-s-saudi-relations-reached-the-breaking-point-11650383578

2) Sino-Iranian Relationship Trumpeted While Implementation Remains Lacking and Beijing Eyes Lucrative Gulf Ties

On 27 April 22, Chinese and Iranian state media touted a visit by Defense Minister Wei Fenghe to Iranian President Ebrahim Raisi in Tehran, where the two sides agreed to step up military cooperation. The agreements reportedly included joint exercises, intelligence sharing, and training cooperation. While the western media made much noise of this as evidence of China’s malign efforts to undermine US hegemony amid the wider backdrop of China’s implicit support for Russia’s Ukraine offensive, a look under the hood of Sino-Iranian ties reveals a less concrete picture. Broadly speaking China’s relations with Iran’s Gulf rivals are far more economically important, and Beijing is wary of shooting itself in the foot by throwing its weight in militarily with Tehran. Putting things into perspective, Sino-Iranian trade in 2020 stood at a mere USD 14.36 billion, while China’s trade with Saudi Arabia and the UAE amounted to USD 65.2 billion and USD 60.2 billion, respectively (see below).

Western pundits were up in arms about the Sino-Iranian Comprehensive Strategic Partnership (“CSP”) penned in 2016 and the more recent Strategic Cooperation Agreement of 2021, with many reverting to the “axis of evil” narrative which aged poorly in Iraq. We note that China has CSPs with Saudi Arabia and the UAE, as Beijing is not seeking the establishment of some Soviet-style bloc, but rather seeks to cooperate with all regional states, including US allies. The China-Iran CSP lacked specific goals, figures, and commitments but unofficial sources claimed that it could involve anywhere between USD 400 and 800 billion worth of Chinese investments in exchange for oil supplies discounted as much as 32% and PLA deployments on Persian Gulf islands. The deal was unpopular in Iran, stoking age-old fears of foreign military presences and the “selling-out” of the country – it was even openly criticized by former president Mahmoud Ahmadinejad.

We point out here that China only invested USD 25.92 billion in Iran between 2005 to 2019, with figures on a downward trajectory – a long way off the triple-digit figures being chucked around in the media. While the figure is slightly higher than Chinese investments in Saudi and the UAE over the same period, a marked shift is occurring whereby investments in these states are rapidly accelerating and have already taken over Iran’s numbers in recent years. Part of this shift can be explained by Beijing’s wariness of violating Iranian sanctions, despite the predictions of western commentators that China would serve as a lifeline to Tehran in this period. While China remains the biggest buyer of Iranian oil – at a steep discount given Iran’s poor bargaining position - Chinese are not being remitted back to Iran in foreign exchange. Beijing has been largely compliant on sanctions as it wished to appease the US in trade deal talks, and obviously, the US is a far more important market than Iran for China’s exports. Even by the Iranian government’s own admission, China has been unwilling to engage in a material deepening of ties until more progress is made on the nuclear agreement.

As for the military sphere, things appear less shaky. China and Iran have indeed conducted joint naval exercises, and the two countries are already, albeit unofficially, engaged in intelligence sharing. However, the rumored PLA deployments to the Persian Gulf islands seem unlikely as they would draw the ire of Riyadh and Saudi, as well as that of the Iranian populace. Notably, Russian aircraft using an Iranian base for refueling in 2018 provoked public outcry, let alone any boots on the ground. Actions speak louder than words in this regard, since 2008, Iran has sought full membership at the Shanghai Cooperation Organization, an economic alliance led by China. Despite Russia’s support, China has blocked this as it seeks to maintain the balance of power among its regional allies in the Middle East and avoid provoking the US in this regard.

We see the much-touted Sino-Iranian relationship as one of greater symbolic value to the two sides rather than Chinese machinations to usurp the regional security and diplomatic order. Tehran benefits from Beijing’s engagement as a means to bolster its own legitimacy on the world stage and project itself as an important regional actor. Beijing has also amplified ties in presenting itself as a credible and valued international partner as part of the wider Belt and Road charm offensive. However, should nuclear talks progress (amid increasing signals in the past few months that this may indeed come to fruition) the stage will be set for deepened cooperation which China’s Gulf allies and the United States are less likely to be irked by.

References:

https://www.bloomberg.com/news/articles/2022-04-28/china-iran-boost-military-cooperation-amid-tensions-with-u-s

https://oec.world/en/profile/bilateral-country/chn/partner/irnf

https://thediplomat.com/2021/04/china-iran-relations-the-myth-of-massive-investment/

https://foreignpolicy.com/2020/12/18/china-wont-rescue-iran/

3) Chinese Investments in Algerian Phosphate as a Means to Reduce Dependence on Morocco?

On 22 March 2022, four Algerian and Chinese firms signed a nearly USD 7 billion deal to relaunch a phosphate mining project in the country aimed at producing about 5.9 million tons of fertilizer annually. Algerian companies Asmidal (a subsidiary of state-owned oil giant Sonatrach) and Manal, along with Chinese companies Wuhuan Engineering Co. Ltd. and Yunnan Tian’An Chemical Co. Ltd., signed a shareholders’ pact for the creation of a joint-stock to begin preliminary activities on an integrated phosphates project. The new company, Algerian Chinese Fertilizers Company (“ACFC”), is 56% owned by the Algerian parties and 44% by the Chinese parties. The targeted level of production from this project would place Algeria comfortably within the top 10 producers worldwide, where it does not currently feature due to lacklustre investment and a poor regulatory climate.

Yunnan Tianan Chemical Co. Ltd. manufactures and distributes diversified chemical products. The Company produces monoammonium phosphate, acids, synthetic fertilizers, and other chemicals. Wuhuan Chemical is involved in fertilizers, acids, pesticides, synthetic materials, and food processing. ACFC is due to exploit the Bled El-Hadba phosphate deposit in Tebessa, transform the product into fertilizer, and export it via dedicated facilities at the Annaba port creating some 6,000 jobs, as well as an additional 24,000 indirectly.

The deal comes more than three years after Algerian state energy firm Sonatrach and Chinese firm CITIC announced a USD 6 billion deal to mine the same deposit. They planned to boost the country's phosphate output from one million to over 10 million tons per year, but the project stalled and a new tender process was launched. The administration of long time president Abdelaziz Bouteflika, who was forced to step down in early 2019 after mass protests against his rule, oversaw the first deal. A second ambitious project which experienced many delays is the joint venture led by Sonatrach to build a phosphate plant in the Tebessa region, which was awarded to Chinese multinational CITIC Construction in November 2018. However, due to infighting within the Algerian regime related to the overthrow of Bouteflika, the parties responsible for the deal were jailed and the project was shelved. Amid Algeria’s complex and opaque political infighting, it looks like new regime insiders have stepped in, and the made-over Algerian government is once again on board.

Algeria could arguably be described as China’s oldest ally in the region. China was the first non-Arab country to recognize the Algerian provisional government in 1958, a historical relationship we covered in a previous post. These ties are bearing fruit, within a decade, China rose to become Algeria’s top trade partner in 2013, surpassing its old colonial master France. Chinese businesses are well-established in Algeria, especially in the construction and energy sectors. Over the past two decades, Chinese enterprises were granted various public development projects valued at more than USD 70 billion. Chinese companies have also been making significant inroads into Algerian military weapons procurement as well as selling surveillance technology to the government. However, as per usual, Beijing rarely puts all its eggs in one basket and has made notable overtures to Algeria’s long-term foe and rival, Morocco.

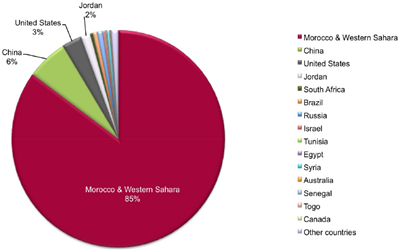

On the subject of Morocco, the phosphate project may be an attempt to diversify away from reliance on Morocco, which has by far the largest phosphate reserves in the world at 70-85% of the total. Granted, it is unlikely that Algeria’s reserves, noting the two countries’ similar geographies, have been fully explored. China is a significant producer itself, but does not have anything like Morocco’s reserves and it is likely that Morocco (and maybe Algeria) will come to dominate the space in the coming decades. As with many commodities, China seeks to multiply its sources rather than relying on one specific supplier and has a rather agnostic approach vis-à-vis Algerian-Moroccan tensions on issues such as the Western Sahara disputed territory. Morocco’s phosphate sector is well developed and the state-owned OCP group already has long-standing joint ventures with US, UAE, and Belgian companies. The importance of OCP Group to Morocco’s economy cannot be understated. It accounts for a quarter of the country’s exports and 3.5% of GDP, raking in USD 5.6 billion of revenue in 2020. If the Tebessa project continues it could very well be a pivot away from OCP Group’s monopoly on this critical commodity.

References:

https://www.statista.com/statistics/681747/phosphate-rock-reserves-by-country/

https://www.statista.com/statistics/681617/phosphate-rock-production-by-country/

https://www.ocpgroup.ma/key-figures

https://www.mei.edu/publications/new-algeria-and-china

https://www.chemengonline.com/algerian-and-chinese-firms-to-jointly-build-7-billion-fertilizer-complex-in-algeria/?printmode=1

https://www.researchgate.net/figure/Remaining-global-phosphate-rock-reserves-as-reported-in-2010-by-International-Fertilizer_fig5_227439251

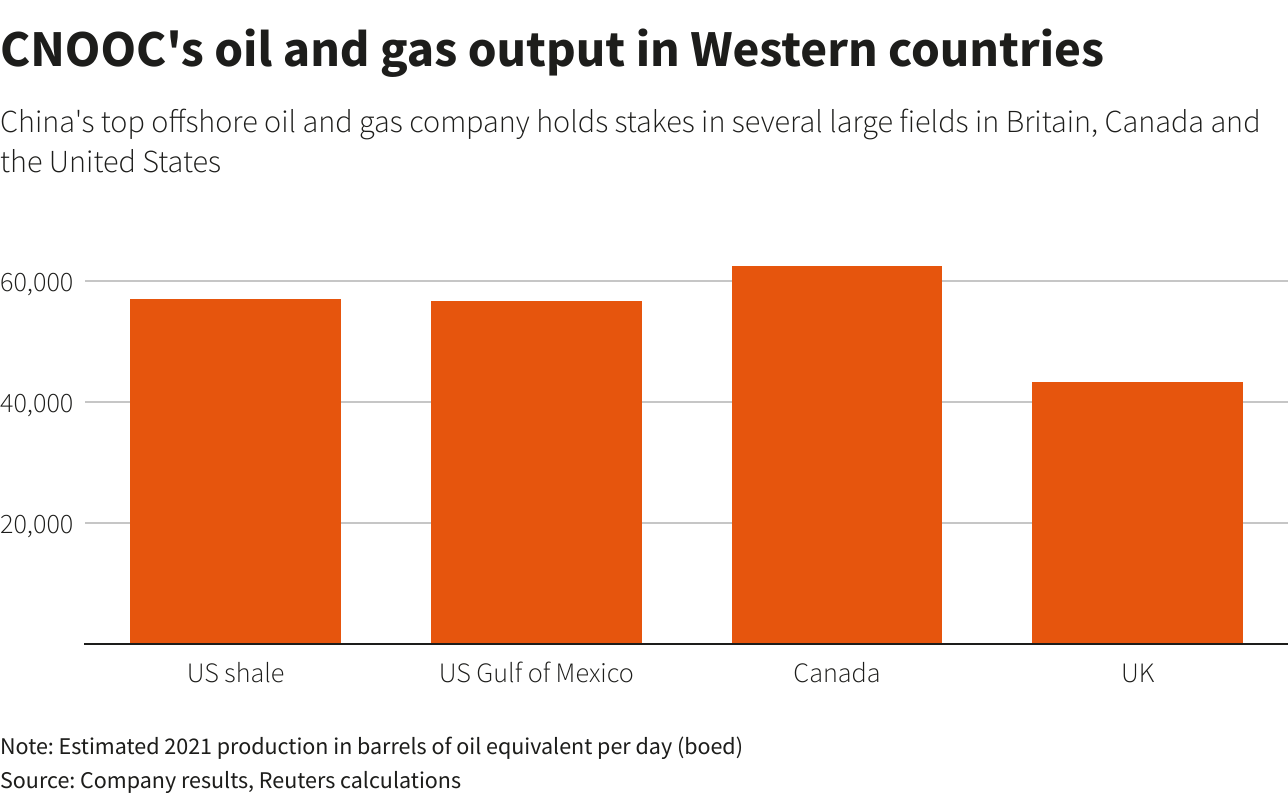

4) China’s Oil Champion CNOOC Resumes Normal Operation of its Overseas Assets in Canada, Britain, and the US While Focusing on Friendlier Neighborhoods

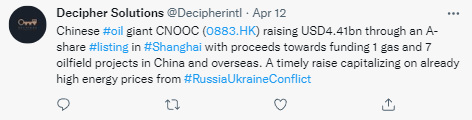

Earlier in the month, we tweeted about CNOOC (0883.HK), China’s top offshore oil and gas company raising USD4.41 billion through an A-share listing in Shanghai to fund its gas and oilfield projects.

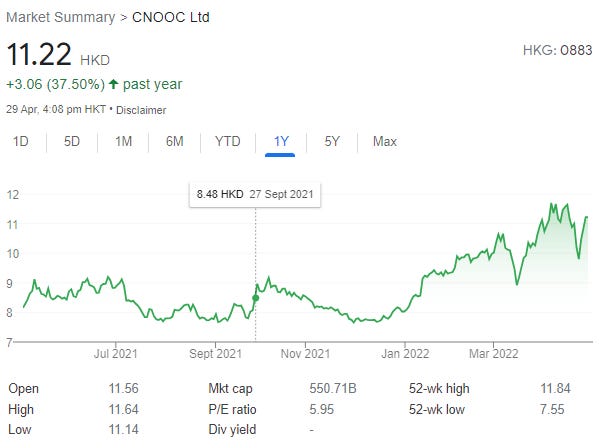

CNOOC’s H-shares have performed strongly since its announcement of a proposed RMB share issue back in September 2021,

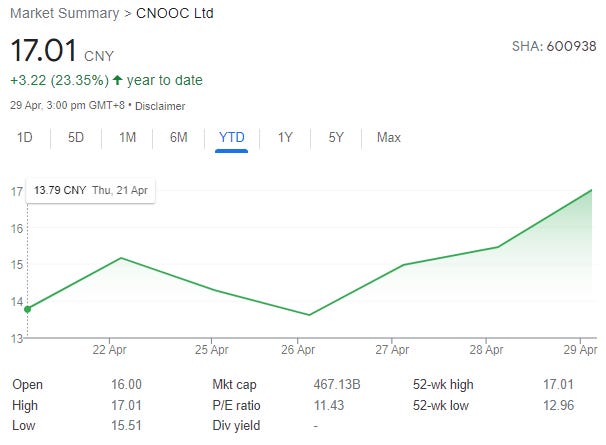

While it’s A-shares saw strong stock buying post-IPO likely on its relatively low valuation, high dividend yield, and high oil prices.

We note that earlier in April, CNOOC mentioned that it was preparing to exit its upstream operations in Britain, Canada, and the US over concerns in Beijing that its assets could be subject to Western sanctions. However, on 21 April 2022, CNOOC reaffirmed the normal operation of those overseas assets.

However, while CNOOC may be maintaining operations in the West, it appears to be prioritizing investments elsewhere. We find it interesting from the perspective that Chinese economic policy stakeholders, including many corporations like CNOOC, are giving much more consideration to its foreign (hard) assets given the West has shown how far its willing to go, having weaponized the global financial system, to contain “bad actors”.

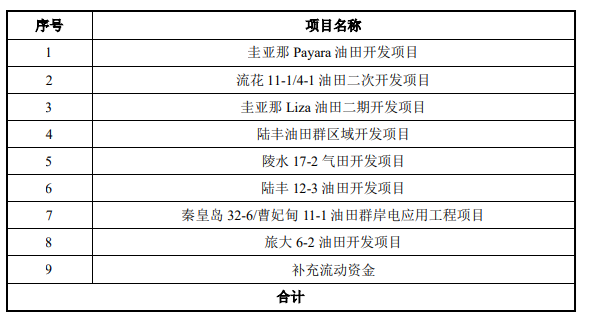

Taking the above into context and as per the table above (summary of use of funds from CNOOC’s A-share issuance [in Chinese]), the company’s overseas gas and oilfield expansion plans are primarily in Southeast Asia and South America, where it can exert much more influence.

References:

https://www.reuters.com/business/energy/exclusive-chinas-oil-champion-prepares-western-retreat-over-sanctions-fear-2022-04-13/

https://asia.nikkei.com/Spotlight/The-Big-Story/China-scrambles-for-cover-from-West-s-financial-weapons

https://www.theedgemarkets.com/article/china-oil-giant-cnooc-soars-44-its-shanghai-debut

http://static.sse.com.cn/disclosure/listedinfo/announcement/c/new/2022-04-11/600938_20220411_3_boGia1za.pdf