Overview and takeaways on Chinese commercial activity in the Middle East and beyond #5

1 May - 31 May 2022

CONTENTS

1) Iraq Shuns Chinese Oil Investments in Likely Short-lived Reaction to Western Pressure

2) Algeria’s State Energy Giant Sonatrach Signs USD 490 Million Production-Sharing Contract with Sinopec

3) Chinese Lithium Miners Turn to Africa Amid Demand Explosion for EVs

4) Egypt Eyes Issuance of Yuan-Denominated Bonds in China

1) Iraq Shuns Chinese Oil Investments in Likely Short-lived Reaction to Western Pressure

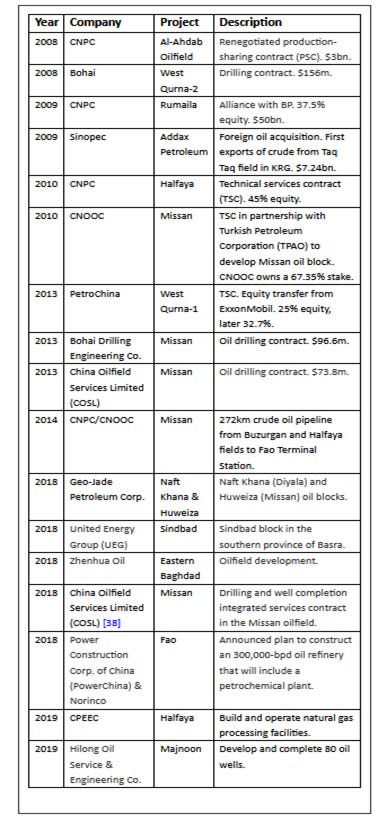

On 17 May 2022, Reuters pointed out that the Iraqi government had shunned three potential deals with Chinese oil companies over fears that this could spark an “exodus” of Western firms. Since 2021, Baghdad has shut down attempts by Russia’s Lukoil (LKOH.MM), British Petroleum (BP.L), and Exxon Mobil (XOM.N) to sell shares in major oil fields to Chinese state-backed firms. We note that China is the largest investor in Iraq, and the country secured the largest (pledged) share of Belt and Road investments (USD 10.5 billion) in 2021.

Reuters quoted well-placed Iraqi oil officials and executives in claiming that Iraq’s Oil Minister dissuaded Lukoil from selling a stake in one of the country’s largest fields, West Qurna 2 (480,000bpd), to Sinopec (0386.HK). Allegedly, Lukoil agreed to this in exchange for regulatory approvals of its development plans at a new field. Oil Ministry officials also vetoed ExxonMobil’s attempt to sell its 32.7% stake in West Qurna 1 (500,000 bpd) to CNOOC (0883.HK) and PetroChina (601857.SS). US State Department officials also allegedly influenced in the decision, over fears that Chinese players could fill a vacuum in Iraq’s oil sector. After Baghdad intervened in West Qurna to find another buyer, no one else was interested and the government is now seeking to purchase the stake itself. As of Jan 2022, the Iraqi government is seeking to buy this stake for USD 350 million).

Iraqi government officials also reportedly dissuaded BP from selling its 47.6% share in the giant Rumaila field (1.5 million bpd) to an unspecified Chinese company. Interestingly, Rumaila is already 46.4% owned by CNPC, so perhaps it was seeking majority ownership of the field. The Rumaila and West Qurna fields account for half of Iraq’s oil output.

As the country has the fifth-largest reserves in the world, these are massive strategic acquisitions, the ramifications, and stakeholders for which go far beyond Iraq’s borders. The interventions also mark a shift in stance after Chinese companies which have grown their Iraq portfolios significantly for over a decade (see below). Iraqi oil officials said Chinese firms have accepted lower profit margins than most rivals. China’s long-standing close relationship with neighboring Iran (see our 4th edition), a key power broker in Iraq’s fractured political arena, have helped Beijing to secure extensive oil interests, particularly in the south where Iranian-backed militias are mainly calling the shots. Generally, foreign oil majors in Iraq are paid a set fee per barrel by Baghdad. Oil companies prefer deals that allow a share in the profits instead, while Chinese firms under state guidance are focused on securing oil supplies for China’s thirsty economy, rather than direct returns for investors.

Source: MEI

With Iraq probably having the most untapped reserves of any OPEC producer, its production has already increased significantly (see below). As one of the few major sources of “new oil” amid sharp price increases, Chinese interest in the country will only increase.

Although Baghdad is attempting to sweeten deals, keeping non-Chinese firms interested appears to be an uphill battle as oil majors grapple with the accelerating energy transition and seek to optimize returns. According to our contacts in Iraq, there are increasingly widespread public calls in support of Chinese investments and denouncing US interventions. Our own social media analysis confirms that pro-China sentiment is significantly widespread with thousands of users engaged in disseminating pro-China content. There is even speculation on the streets that the US actively supported anti-government protests in 2019-2021 in order to prevent a further warming of ties with Beijing. Whatever the truth, optics are important. Given the limited interest of non-Chinese firms to do business in Iraq, it seems Baghdad will eventually have to turn to Beijing to ensure its petrodollars, from which 90-97% of the state budget is funded. China is Iraq’s biggest oil buyer – as long as Baghdad needs to cough up the vast sums needed to keep the peace in the country and level up infrastructure through BRI funding, it will likely turn back to its most reliable foreign buyer.

References:

https://www.mei.edu/publications/china-iraq-relations-poised-quantum-leap

2) Algeria’s State Energy Giant Sonatrach Signs Contract with Sinopec

On 29 May 2022, S&P Global reported that Algeria’s state energy giant Sonatrach and its Chinese partner Sinopec had signed an oil production sharing contract (PSC) on the Zarzaitine Concession in the Illizi Basin. The site is located near the border of Libya, in the far east of Algeria. The deal is expected to bring in around 95 million barrels per annum into the market as Algeria, an OPEC producer looks for additional investment into its energy sector. The PSC is also worth USD 490 million. Both sides agreed to revamp existing surface facilities, drill 12 new development wells, workover on six existing wells, and tackle gas flaring in order to lower carbon emissions.

It is noteworthy that Sinopec has long been a partner at the Zarzaitine field. The Chinese company signed an agreement with Sonatrach in 2003 to increase its recovery rate from 28,000 barrels p/day to 50,000 by 2023.

Also, this is not the only instance where Sonatrach has done business with Sinopec. We reported back in our 2nd edition in February 2022 that the Algerian company had signed storage and liquefication contracts with units of Sinopec. Prior to that, both companies also signed several memorandums of understanding (MoUs) in 2021. However, apart from the aforementioned agreement, moving from MoUs into PSCs has been a slow process as expected given size and scale of these contracts.

Consistent with the narrative we discussed in February 2022, we will continue to see key Chinese energy and infrastructure state-owned enterprises closing massive deals in both sector in line with Beijing’s Belt and Road initiative. We continue to watch bilateral developments closely…

References:

https://www.energyvoice.com/oilandgas/africa/ep-africa/415548/sonatrach-sinopec-psc-pipeline/

3) Chinese Lithium Miners Turn to Africa Amid Demand Explosion for EVs

In line with our focus on Chinese commercial expansion in the Middle East and the wider developing world, we highlight the ongoing trend of overseas acquisitions targeting lithium and other key commodities in electric vehicle manufacturing. On 24 May 2022, Mining Weekly reported that China’s Zhejiang Huayou Cobalt (603799.SZ) was planning to invest USD 300 million in developing a newly acquired project in Zimbabwe. Huayou Cobalt recently purchased the mine, just outside of Harare, for USD 422 million from Australia-based Prospect Resources (PSC.AX) and Zimbabwean stakeholders. A Huayou Cobat announcement, the investment would target production of 400,000 tonnes of lithium concentrate per annum, placing it among the top 10 largest lithium mines in the world. First deliveries from the mine are expected in 2023.

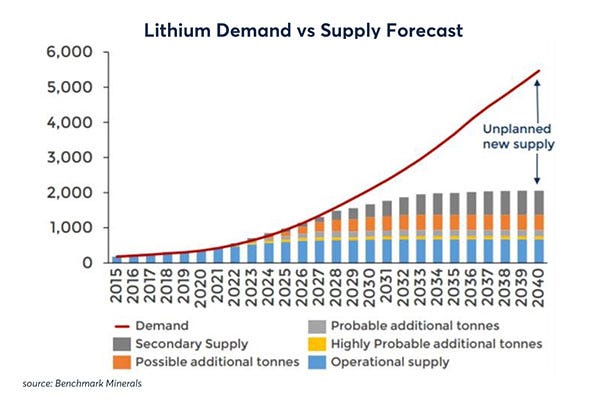

China’s EV market dwarfs that of any other country and is expanding at breakneck speed due to political and economic incentives offered to both local governments and consumers. According to a May 2022 report by Gavekal Research, China already refines 60% of the world’s lithium, controls 77% of global battery cell capacity, and 60% of global battery component manufacturing. As China has established itself as a global lithium processing and EV manufacturing hub, its companies are becoming increasingly active in acquiring upstream mining operations, a trend we touched upon in our 1st edition.

These deals have seen massive projects taking off in South America and Australia, and now evidently Africa. Several factors are at play here, the US has lost many friends in the developing world due to harsh trade policies and interventionalist foreign policy. Chinese companies enjoy firm state backing and access to cheap funding. While Western governments and companies are now waking up to the strategic nature of lithium production, it will take them some time to catch up with their Chinese competitors. All of this comes amid the backdrop of soaring demand for lithium ion batteries worldwide, with the International Energy Agency forecasting a 20-fold rise in lithium sales by 2030.

Global demand and supply for lithium are in approximate equilibrium for now (although this hasn’t stopped the commodity’s price from skyrocketing recently). Given the length of time it takes to plan and implement new mining projects, demand is forecasted to far outstrip supply in the coming decades.

As such, we are optimistic that investments in Chinese major lithium miners and producers could pay off in the long term, with notable picks including Ganfeng Lithium (002460.SZ), Tianqi Lithium (002466.SZ), China Molybendum (3993.HK) Jiangsi Special Electric Motor (002176.SZ), and Sichuan Yahua Industrial Group (002497.SZ).

References:

https://www.statista.com/chart/23808/lithium-ion-battery-demand/

https://www.barrons.com/articles/china-ev-batteries-lithium-mining-51652889888

https://www.fpri.org/article/2022/03/chinas-rare-earth-metals-consolidation-and-market-power/

4) Egypt Eyes Issuance of Yuan-Denominated Bonds in China

Another piece of news that caught our attention this month was Zawya reporting on 12 May 2022 that Egypt was eyeing the issuance of yuan-denominated bonds in China. Details regarding the issuance remain light with no information regarding the amount to be issued, maturity, coupon, and yield.

This is of course not the first time Egypt pursued offshore bond financing. Cairo has issued several bond issuances in recent years as means to help finance its infrastructure spending spree. In Asia, Egypt was the first country in the Middle East last year to issue USD 500 million worth of 5-year 0.85% annual coupon bonds, denominated in Japanese Yen in the Japanese market. However, the yield did seem surprisingly low for a frontier market. In any case, we would suspect yuan-denominated bonds to be more attractively priced. Egypt has been harder hit by global economic shocks, particularly amid backdrop of the Russian-Ukraine conflict, which have pushed domestic prices of food commodities and oil significantly higher.

Egypt’s finances have been distressed for some time now. In 2021, the country’s budget deficit and public debt amounted to 9.5% of GDP and 93.5% of GDP respectively, which are unsustainable and can leave Egypt vulnerable to further economic and market shocks. According to the Egyptian Draft Budget for 2022-23, the country aims to reduce its public debt to GDP ratio to 82.5% by June 2025 (Statista forecasts are slightly more optimistic than the government). Cairo also plans to raise revenues by 13-15% in 2022-23 and reduce state spending. Given the macroeconomic conditions facing Egypt, it will be difficult to see much reform in its subsidies scheme. Food subsidies are costing around USD 5.5 billion now with even higher food prices expected over the course of this year. It is worth mentioning that Egypt is one of the top wheat importers globally and urban inflation rate has already surged to 10.5% in March 2022, the highest rate in almost 3 years. To add to the country’s distress, commodity spikes are leading to higher fuel prices and the Central Bank of Egypt also devaluing its currency (EGP) by around 15% against the dollar in March 2022 is not having the requisite effect.

Source: Statista

The Central Bank move was initially designed to make exports cheaper, maintain liquidity of its currency, and attract inflows back into Egypt. However, currency depreciation is also leading to high imported inflation, which is resulting in Cairo paying for almost twice the cost of imported commodities (prices exacerbated by the Russian-Ukraine conflict). The Egyptian Central Bank has already hiked its benchmark interest rate by 2 percentage points to 11.25% this month. Further increases are expected in order to slow down inflation and protect its currency, but the effects of which won’t be felt in the short to medium term.

Cairo has a long uphill battle to climb being heavily reliant on imports, which makes up 18.1% of GDP relative to its exports only amounting to 10% of GDP in 2021. It also remains a large net energy importer despite discovering new natural gas reserves. On top of its economic crisis amid high debt levels, government spending priorities have largely been directed towards large scale infrastructure projects that have limited short term payoff. Its nearly-complete USD 50 billion New Administrative Capital project is currently facing funding shortfalls, while the USD 3 billion Suez Canal expansion has generated a limited return on investment.

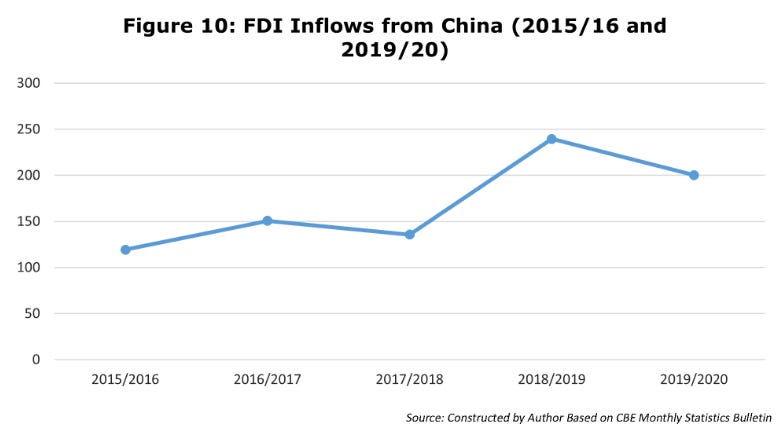

China has been a major investor in Egypt since signing a strategic partnership in 2014 with FDI inflows increasing by 68% between 2015-16 and 2019-20. Going forward, we expect China’s investments to continue to focus on new capital infrastructure projects. Given the relatively easier terms of payment offered by Chinese state-owned firms, often acting on political imperatives, Cairo will likely continue to rely on them for many of its major infrastructure projects.

References:

https://countryeconomy.com/key-rates/egypt

https://www.aljazeera.com/opinions/2021/7/5/why-is-egypt-building-a-new-capital

https://gulfbusiness.com/egypt-reaches-8-5bn-funding-goal-suez-canal-expansion/