Overview and takeaways on Chinese commercial activity in the Middle East and beyond #3

1 Mar - 31 Mar 2022

CONTENTS

1) Increasing Downstream Cooperation Between Saudi State-Owned Firms and Chinese Counterparts

2) China Steps in to Engage Taliban in Pursuit of Mineral Wealth and Security Guarantees

3) Yemeni Houthi Attacks on Saudi Chinese Oil Facilities Pose Challenge to Beijing’s Hands-off Stance

1) Increasing Downstream Cooperation Between Saudi State-Owned Firms and Chinese Counterparts

On 10 March 2022, Chinese regulators approved a joint venture (JV) between Saudi Basic Industries Corp (2010.SE, “SABIC”) and Fujian Petrochemical Industrial Group (“FJPEC”). SABIC is a state-owned company and the world’s fourth-largest chemical company with revenues of USD 46.6 billion and profits of USD 6.16 billion in 2021. Fujian Petrochemical Company (FPCL), a 50:50 JV between FJPEC and Sinopec, owns a 50 percent stake in Fujian Refining & Petrochemical Company Ltd (FREP), a joint venture with ExxonMobil China (25%) and Saudi Aramco Sino Company (25%), according to FREP's website. Saudi-state-owned Aramco’s stake in FREP no doubt facilitated this JV with another Saudi government-owned company.

The SABIC-FJPEC JV has been in the works since 2018, and now with a final sign-off by Beijing will involve a USD 6.33 billion investment in an ethylene plant at the Gulei petrochemical facility in Fujian producing 1.5 million tons per annum of the hydrocarbon. Ethylene, derived from oil or natural gas, is described as the “world’s most important chemical” and is used in the production of plastic, detergents, antifreeze, polyester, and synthetic rubber, among other applications.

In another significant sign of increased Sino-Saudi cooperation in China’s downstream sector, Aramco and Sinopec signed an MOU in March 2022 on downstream collaboration and support for FREP (introduced above) to expand capacity. The other Sinopec-Aramco JVs are Sinopec Senmei (Fujian) Petroleum Company (SSPC) in China and Yanbu Aramco Sinopec Refining Company in Saudi Arabia.

With Saudi petrochemical companies becoming much more active in downstream investments in China in recent years, after previously acting mainly as upstream suppliers, we believe the trend of Saudi involvement in JVs will become increasingly relevant and may serve as a catalyst for publicly traded stocks in SABIC and Aramco. China is now Saudi Arabia’s main oil export market, having long replaced the US in this regard, Saudi conglomerates are now realizing the strategic value of betting big in this crucial market, and more acquisitions and JVs will follow.

References:

2) China Steps in to Engage Taliban in Pursuit of Mineral Wealth and Security Guarantees

On 24 March 2022, China’s Foreign Minister Wang Yi made a surprise visit to Afghanistan to meet with the new Taliban government. While western countries were grudgingly moving towards accepting the Taliban as a fait accompli, much noise was made in recent weeks about the group’s broken promise to reopen high school education for girls. As per its usual modus operandi, Beijing has only paid lip service to such internal matters, with economic and security issues at the front and center of Wang Yi’s visit, although Wang Yi did make token mention of rights issues. While China has not overtly recognized the Taliban government, it has maintained its embassy in Kabul and after the meeting, Wang Yi said China would recognize the Taliban “when conditions are ripe.” Nevertheless, come what may, any recognition by Beijing will be hindered by ongoing western sanctions, meaning few banks will deal with the Chinese government, and so it seems to be pursuing a more inclusive international process that will bring international recognition to the Taliban, albeit under China’s auspices.

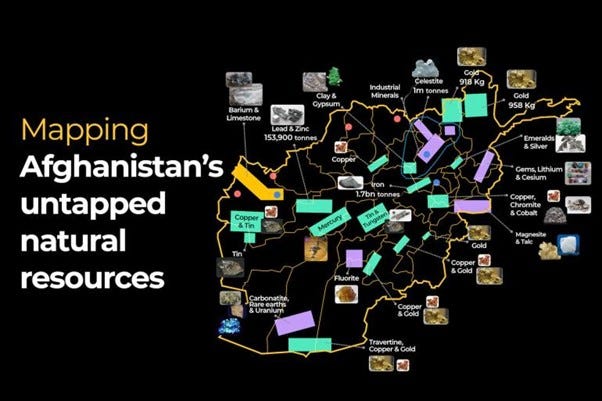

China is interested in Afghanistan’s mineral wealth and strategic position as a transit hub. In particular, the country has untapped deposits of key metals used in electric vehicle production and other high-tech industries, such as copper, lithium, and cobalt, with some estimates valuing these deposits at USD 3 trillion. One thing is for certain, the Taliban won’t be rushing to make deals with western companies due to ongoing animosities. The feeling is mutual, the bad press that would arise from western companies doing business with the repressive Taliban regime may be too toxic to handle.

While Chinese companies are already involved in some investments, it should also be noted that security concerns are holding back the kind of large-scale investments that would allow it to “step into the vacuum” left by the US, despite many western media outlets oversimplifying Beijing’s intentions as just this. In an illustrative example, in 2008 a consortium of Chinese companies took a 30-year lease for the largest copper project in Afghanistan, Mes Aynek, and to date no work has commenced due to security and infrastructure issues. This is despite the site holding deposits with an estimated value of over USD 100 billion. Such constraints have not stopped Chinese investments in places like Sudan and the Congo, but cooperative local governments are needed to guarantee security, and Beijing-Taliban relations don’t seem to have matured to that point yet.

Beijing also appears to be courting the Taliban due to security concerns. Chinese diplomats have repeatedly sought assurances that the Taliban would not allow Uyghur separatist movements to operate in its territory. The Taliban may well be on the same page here, the overseas East Turkestan Islamic Movement, which has long been fighting a low-level insurgency against the Chinese government, threw its lot in with a local Islamic State affiliate which is a mortal enemy of the Taliban. Chinese companies have also had their fingers burned in Pakistan with attacks launched on their employees by groups based in Afghanistan, hence China may seek assurances from the Taliban that these groups will be reined in.

It does not appear that Beijing wants to ice the West out of Afghanistan’s reconstruction process. In fact, it has called on the West to take primary responsibility for reconstruction. However, China prefers to have the US and its allies under the umbrella of its own peace process, with the US having cancelled its own set of talks to be held in Doha due to the female schooling issue. As noted above, China needs western engagement in talks with the Taliban, as unilaterally recognizing the new government will do little to facilitate trade due to sanctions. In late March 2022, Wang Yi hosted Afghanistan-related talks with Russian Foreign Minister, Sergei Lavrov for his first overseas strip since the invasion of Ukraine. The meetings in Anhui province were also attended by representatives from the Taliban, neighboring countries, and the US. Notably, meetings involving US representatives were not attended by Lavrov or Wang Yi, in what may be a telling sign of the pecking order.

References:

https://www.aljazeera.com/news/2021/9/24/mapping-afghanistans-untapped-natural-resources-interactive

https://www.nytimes.com/2010/06/14/world/asia/14minerals.html?hp=&pagewanted=all

https://thediplomat.com/2022/03/chinas-foreign-minister-makes-surprise-stop-in-afghanistan/

https://thediplomat.com/2022/03/chinas-foreign-minister-makes-surprise-stop-in-afghanistan/

https://www.reuters.com/world/china-hosts-russia-us-officials-talks-afghanistan-2022-03-30/

3) Yemeni Houthi Attacks on Saudi Chinese Oil Facilities Pose Challenge to Beijing’s Hands-off Stance

On 20 Mar 2022, Yemen’s Houthi insurgent group announced that it had conducted missile strikes on oil facilities in Saudi Arabia. The strikes hit a petroleum products distribution terminal in the southern Jizan region, a natural gas plant, and the Yasref refinery in the Red Sea port of Yanbu. Houthi drone and missile strikes on Saudi and UAE oil infrastructure are a regular occurrence and are a form of economic warfare in response to Saudi-led campaign against the Houthi rebels dating back to 2015. We highlight this incident because the Yasref refinery, where production was temporarily reduced, happens to be a JV between Sinopec and Aramco and the strike may influence China’s generally muted stance on the Houthi movement. Beijing may also be increasingly uneasy as Houthi rebels also pose a threat to the Bab al-Mandab strait, where all marine traffic going through the Suez Canal needs to pass. Another key factor here is China’s increasingly close political and economic ties with Saudi Arabia and the UAE, a trend that we have discussed extensively on this blog.

China officially recognizes the Saudi-backed and anti-Houthi government in Yemen. The Yemeni government has lost much of the country’s territory and economic assets to the Houthis, which means overtly taking sides in this conflict may not pay off in the short term. Simply backing the Yemeni government will not resolve the conflict, as Saudi and UAE military interventions have led to high civilian death tolls and massive infrastructural damage - the two Gulf powers are detested by large swathes of Yemen’s population. A further complication to this matter is staunch support to the Houthis provided by Iran (a key ally of Beijing), with further Chinese intervention likely to upset Tehran. China’s primary interest appears to be security for its Gulf energy suppliers and is likely to be nervous about increased Houthi attacks on oil export infrastructure. As recently as 2021, Beijing has reiterated its recognition of the Yemeni government and condemned Houthi attacks on Saudi territory. For now, it seems that China will continue to act as a mediator in the conflict while diplomatically backing the Yemeni government, but should attacks continue to directly affect Chinese oil interests in Saudi Arabia, this may well tip the balance.

References:

https://www.ansarollah.com/archives/505900

https://insidearabia.com/chinas-gulf-relations-and-calculated-stance-on-the-yemen-war/