Overview and takeaways on Chinese commercial activity in the Middle East and beyond #8

1 Aug - 31 Aug 2022

CONTENTS

1) China Stacking the Deck in the Global Tech Race

2) Chinese Automakers Race Ahead in Gulf Markets With an Eye on EV Growth Potential

3) Iran Approves Regulation on Crypto Payments for Imports

1) China Stacking the Deck in the Global Tech Race

For the first time in 30 years, South Korea quietly recorded an unprecedented three-month long trade deficit with China, with shortfalls of over USD 1.1 billion, USD 1.2 billion, USD 570 million, and in May, June, and July respectively. The last time South Korea registered a trade deficit with China was in 1994 and there are seemingly more structural causes driving the downturn. If we observe the top trade items, 16.5% of Korean imports from China were semiconductors, 10.3% fine chemicals for batteries, and 5.5% computers. Seoul’s technology sector has long been viewed as the economy’s strong point, but at the crux of Korea’s trade deficit is China’s state-led industry challenging the traditional dominance of the former’s high-tech products.

Analysts were quick to play down China’s competitiveness in the semiconductor industry relative to Korean products in the case of high-end chip market. Taiwan’s TSMC and Korea’s Samsung Electronics are racing to produce 3-nanometer chips, while China’s state-owned SMIC only has a single 14-nanometer plant and most Chinese players are capable of only 28-nanometer and above. However, it was reported that SMIC had already advanced its technology to a quasi-7-nanometer process.

Ongoing US restrictions have limited many Chinese companies to focus on designing lower-end semi-conductors, which has led to a 33% increase last year to over 359 billion chips manufactured. The Chinese government has been heavily subsidizing semiconductor companies to build factories as part of its “Made in China 2025” policy aimed at achieving 75% self-sufficiency in chips. Beijing plans to invest CNY 1 trillion (USD 145 million) into the sector alone in this period’s Five-Year Plan (2021-2025), which includes integrated circuits as one of the seven technologies, as well as AI, aerospace, and quantum computing.

The size of China’s semiconductor market reached approximately USD 187 billion in 2021, representing a 17% self-sufficiency rate. The Wall Street Journal reported that China will lead the world with 31 new factories, surpassing Taiwan (12) and the US (19) by 2024. In typical Chinese fashion, Beijing is looking to prop up its manufacturing base to squeeze out foreign tier two or three wafer foundries from export markets. This strategy will pressure existing (overseas) mature process manufacturers and to a lesser extent the likes of TSMC, Samsung, and Intel, which are more advanced in their technology.

The shifting dynamics of Korea-China imports are a tell-tale sign of the active progress made by Beijing in the chip trade. However, it is noteworthy that leading Korean chipmakers are somewhat stuck between a rock and a hard place in the wake of the US Chips Act passed in late July. The Act envisages USD 52 billion in grants to support advanced chip manufacturing in the US and contain China’s advanced chip capacity for 10 years. South Korea’s re-calibration of trade strategy to the US will be tough given heavy investments in China, but also the country’s economic reliance on chips. Time will tell, but it looks like South Korea is becoming a structural trade debtor to the Chinese. We all know how that story goes – China is particularly patient and perhaps we may see a shift in geopolitical loyalties over time?

How can we reconcile this interesting trend with the Middle East? Well simply put, semiconductors are an essential component of any industrial or electronic application. Gulf states like Saudi Arabia have ambitious goals to digitally transform their Information and Communications Technology (ICT) sector as part of its Vision 2030 plan. With the US’s receding influence in the region, Beijing is set to capitalize both economically and politically by integrating data, cyber and technology into Middle East relations. A good example of the semiconductor effect on the downstream is Huawei entrenching itself in the Middle East from being a low-cost ICT vendor to a full-integrated technology partner with Egypt, Morocco, and the GCC states across a wide array of functions including surveillance, telecoms infrastructure, and cloud computing. Another interesting growth area for Chinese chip manufacturers is increasing sales of Chinese EV manufacturers in emerging markets, a trend also pertinent in the Middle East which we discuss below.

One thing is for certain, while it is too early to tell whether Chinese chip manufacturers can close the gap on high end products, their entrance into the lower and medium tiers is already setting alarm bells off in Korea, Taiwan, and even the US. This means that stocks like SMIC (0981.HK) are interesting picks and worth a closer look in future editions.

References:

https://thediplomat.com/2022/08/chinas-semiconductor-breakthrough/

https://www.wsj.com/articles/china-bets-big-on-basic-chips-in-self-sufficiency-push-11658660402

https://www.ft.com/content/73d0ce63-0b2a-47d7-9d97-9ecf367ef924

https://asiatimes.com/2022/09/china-catches-cold-south-korea-gets-the-flu/

http://www.businesskorea.co.kr/news/articleView.html?idxno=99598

https://www.ft.com/content/0b997942-93bd-4a67-9784-928af2641738

2) Chinese Automakers Race Ahead in Gulf Markets With an Eye on EV Growth Potential

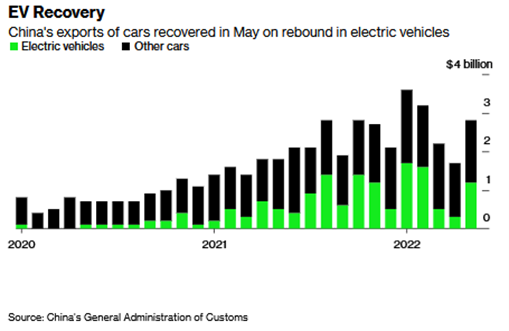

This month, Arabic language media outlets circulated an article claiming that Chinese cars were taking the Gulf countries “by storm”, and that in some countries, sales of China-manufactured vehicles were growing by 35% annually. The article quotes official statistics in noting that Chinese autos now make up 10-15% of vehicle sales in Gulf states, with this figure reaching 20% in the UAE. Our research also found that Saudi Arabia was China’s largest auto export market by volume with nearly 100,000 vehicles shipped in 2020, trailed by Egypt and Bangladesh. Interestingly, the likes of Geely (0175.HK) and BYD (1211.HK) have long exported to the Middle East since the early 2000s, but this tended to be budget models competing on price. A notable trend we are seeing is a greater penetration of Made in China luxury vehicles and electric vehicles (“EVs”) in the Middle East, where there are now over 20 Chinese brands operating. This comes as perceptions of China manufactured goods among the region’s population are gradually improving and Chinese automakers are facing sluggish sales at home due to various macro factors. Gulf states also have some of the highest per capita car ownership rates in the world. Furthermore, the Middle East (particularly the Gulf) represents an attractive market as its governments maintain warm ties with Beijing whereas many other export markets are impacted by negative public perceptions of China and hostile trade policies.

Source: Arab News

Chinese automakers are increasingly looking to establish a manufacturing presence in the region as well. For example, last year EV Dynamics (Holdings) Limited (0476.HK) announced that it would enter a JV to establish manufacturing operations in the UAE. In December 2021, the Egyptian government announced that a state-owned auto manufacturer would link up with an unnamed Chinese company to develop and manufacture a low cost EV. If this takes off, a significant market could be unlocked as just 350 of the 5 million cars on Egypt’s road are EVs.

Speaking of EVs, we see this as a crucial growth area for Chinese manufacturers, which enjoy policy support to boost sales at home and abroad as Beijing seeks pole position in this rapidly expanding and strategically important sector. Saudi Arabia seeks to have 30% of auto sales made up of EVs by 2030, along with a host of other similar goals by other Gulf states. One may wonder why the oil-rich region, with its subsidized fuel prices and a penchant for gas-guzzling SUVs may be turning to EVs. While it is possible that Gulf monarchies are finally getting on board with climate change and looking to cut emissions, the truth may be somewhat simpler. Given soaring oil prices and what may be a limited time frame for oil exporters to shore up finances in the one or two decades before EVs and renewable energy start making a serious dent in global oil demand, they are looking to cut local consumption in favor of exports. This has involved significant rollbacks of fuel subsidies and small but promising signs of policy support for EV transition.

In Saudi Arabia, Chinese manufacturers of both EVs and traditional automobiles are prioritizing the lower to middle-income segment. While European and Japanese automakers will continue to dominate the luxury market for the foreseeable future, lower-tier segments appear within reach, especially for EV manufacturers. Technically speaking, EVs are much less technologically complex to manufacture compared with traditional automobiles, meaning that the learning curve for Chinese manufacturers has been significantly less steep with exports growing rapidly, and in some cases, their technologies rival those of their western counterparts. This has allowed China to capture a 60% share of global EV exports, although we note that vehicles produced by the likes of Tesla in China are also included in this figure.

As in many other high-tech industries, Chinese companies are not necessarily trying to displace the top high-end players (for the short term), but rather they recognize that the ability to produce at large scale, decent quality, and lower price points positions them strongly in the lower to mid-tier segments. This advantage lends itself naturally to a focus on emerging market economies, where as mentioned earlier, conditions for Chinese exporters are less hostile. Furthermore, it is these markets where consumption is growing rapidly from a low base and where high-profile EV manufacturers may not have prioritized sales and marketing efforts. The Middle East is a case in point and we will be watching moves by big Chinese EV players in this space and wider emerging markets in the months to come.

References:

https://www.gccbusinessnews.com/chinese-automobile-brand-exeed-plans-to-venture-into-gulf-markets/

https://www.ft.com/content/c252cca0-07a6-4dc7-be25-09ac5bb658ce

https://akhbaralsin-africia.com/2022/08/15/24248/

https://www.arabnews.com/node/1901251/business-economy

3) Iran Approves Regulation on Crypto Payments for Imports

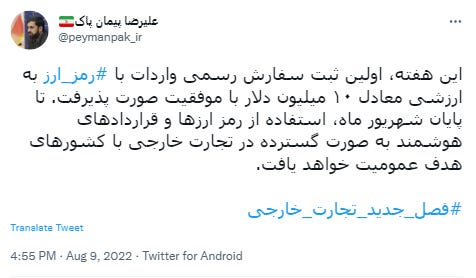

Reza Fatemi Amin, Iran’s Minister of Industry, Mines and Trade (IMT) announced during an automobile expo in Tehran that the Iranian government has approved a legislative reform on the use of cryptocurrencies in trade and commerce. Underlying issues, costs, and logistics pertaining to mining activities have also been finalized.

The Minister confirmed in a tweet on 9 August 2022, a week prior to the expo that Iran’s first-ever import order of over USD10 million worth of vehicles was paid in cryptocurrency (although the currency was not specified, it was likely in bitcoin).

It is also worth mentioning that the IMT issued operating licenses to 30 crypto mining farms back in June 2017. To date, there are reportedly almost 2,500 licenses issued for new mining activities, in a softening stance towards crypto mining. The Minister also pointed out that the country plans on a wider implementation of crypto and smart contracts starting in September.

These developments do not come as a surprise given the ongoing international trade sanctions placed on Tehran for its nuclear program. In addition, it could provide the government with another source of tax revenues. Licensed miners operating in Iran reportedly account for around 4-4.5% of the total hashrate (a measure of computational power p/second used when mining) over the past year. The country sits in the top 10 globally in terms of revenues gained from license fees and premiums on power supply. However, Iran’s mining hashrate seemingly dipped towards the start of 2022, likely over increased global energy costs, and processing power required to mine bitcoins. It would be interesting to see how Iran has fared in the past 9 months when we get our hands on more updated statistics.

While Iran already engages in multi-currency trade between its close partners, namely China and Russia, crypto payments offer Iran another direct outlet to bypass the traditional banking system, where unauthorized transactions can be blocked at the whims of the US and its allies.

Iran’s increased usage has limited impact with regards to the wider implications for the price of bitcoin, which is still highly correlated with the S&P 500 and NASDAQ, and US Fed policy movements. Reversing policy tightening or some other liquidity injection are positive for risk assets; a potential possibility in Q422 if the Fed pivots on the back of a continually weakening US economy.

References:

https://coinculture.com/au/policy-regulation/irans-new-crypto-law-to-circumvent-u-s-sanctions/

https://cryptopotato.com/iran-formally-approves-the-use-of-digital-assets-for-imports/