Roving around Riyadh – A look into a kingdom forging its future through reform (Part 2)

Work trip to Saudi Arabia sheds light on reform progress, geopolitical shifts, and consumer habits.

From September to October, Desertfox spent 1 month in Riyadh, the capital of Saudi Arabia.

This is the final piece concluding a two-part Series covering Desertfox’s recent trip to Riyadh, during which he gained interesting insights into how Saudi Arabia’s soft power push translated to real life experience working with the Saudi public sector, how this might benefit a Hong Kong-listed proxy, and the notable rise of Chinese automakers on the Kingdom’s streets.

In Part 2 of this series, we look at how Saudi consumer habits translate into retail real estate in the FCMG space and how one European player is cornering the Kingdom’s vast food delivery market. Also in this instalment, we delve into the mechanics of investing in the Saudi stock exchange and an exciting new ETF that could offer exposure to this emerging market.

Local hypermarkets illuminate consumer habits and shelf real estate practices

During my limited free time at the conference, I had the opportunity to visit several local hypermarkets. The hypermarket segment in Saudi Arabia is mature, with an estimated annual retail value of approximately USD 5 billion. However, its growth has been relatively stagnant in recent times, so we won't delve into extensive details here. The major players in this segment include Pandra Retail Co., subsidiary of Savola Group Company (2050.SE) holding a 31.7% market share, and privately-held BinDawood Group, holding a 20.2% market share.

One aspect that caught my attention was the abundance of junk food available in the hypermarket. While it shouldn't have been surprising given that Saudi Arabia has some of the highest obesity and diabetes rates in the world, it was still noteworthy. Coming from cities like Hong Kong and London, where grocery stores often have limited space, I was surprised to see the significant shelf space dedicated to individual brands. However, this often came at the expense of other brands, and I suspect that premium brands may be providing incentives for such prominent placement.

Another observation I made was the significant number of local women working at the checkout counters. Traditionally, these positions were filled by low-paid migrant workers. This change reflects the social reforms taking place in the Kingdom, where efforts to empower and provide employment opportunities for local women are being implemented at a grassroots level.

As is often bemoaned by foreign expats in the Kingdom, you won’t find any alcohol section in hypermarkets, nor anywhere else for that matter. The Kingdom is officially bone dry, although that’s not to say a healthy market for bootleg booze exists. Judging by the exploits of wealthy Saudi travellers in European capitals, one can hardly say that the locals aren’t partaking either.

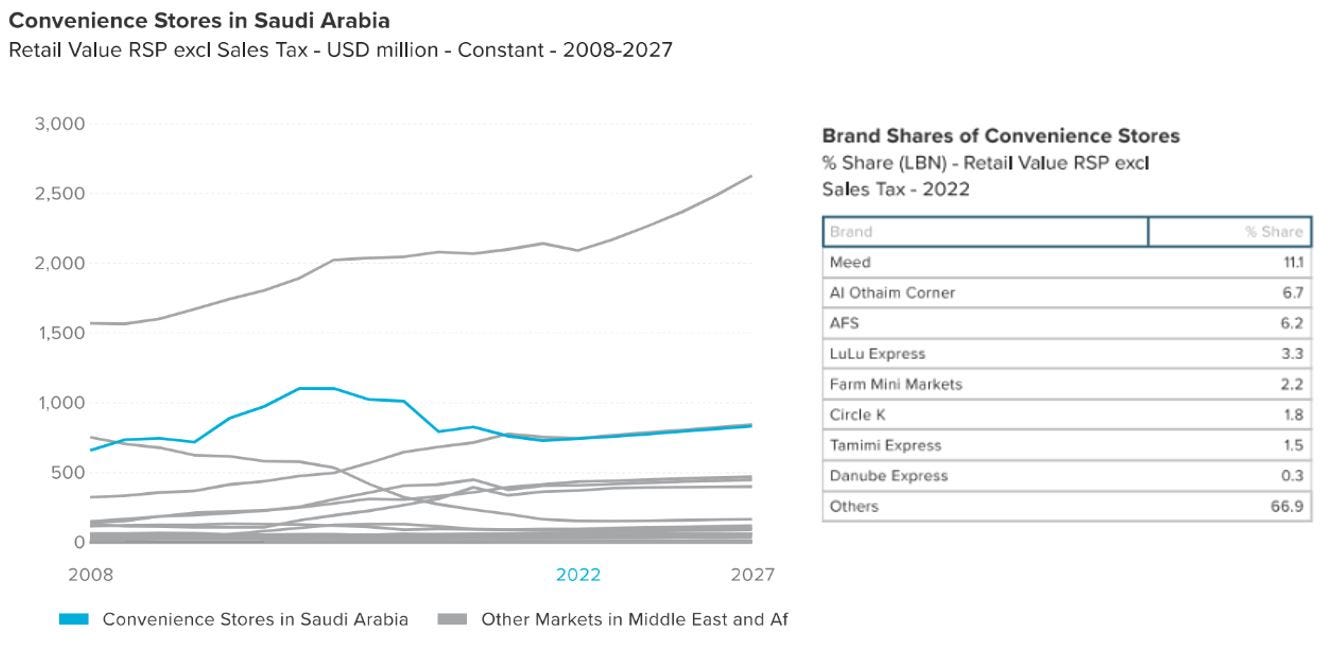

Convenience stores few and far between, but this could change quickly

Riyadh, like many other car-dominated cities, heavily relies on private vehicles, and pedestrians and public buses are relatively uncommon sights. Although Riyadh has a large metro project under construction, it may take some time for last-mile connectivity to develop fully, and cultural aversions to public transport may need to be addressed before widespread adoption occurs. Similar to many large cities in the US, street life in Riyadh revolves around drive-thru locations or places with ample parking space. This may explain the lack of convenience retail along major roads, with hypermarkets serving as primary destinations for grocery shopping, as observed.

However, with the increasing number of women joining the workforce and the post-pandemic shift back to offices, there is a missed opportunity to cater to the evolving needs of the population. Convenience store segments have thrived in many other car-dominated cities worldwide, often integrating parking spaces or strategically locating themselves at gas stations. This, however, is relatively rare in Riyadh, where major global players like Circle K have only a limited presence, with just five locations in the Kingdom. Part of the challenge lies in cultural factors, as the approximately 50,000 individually operated corner stores across the Kingdom often rely on low-cost migrant labour to take orders from customers in their vehicles. However, major players that prioritize enhancing in-store experiences could potentially encourage Saudis to venture out of their vehicles and spend more time in convenience stores.

However, with women increasingly joining the workforce and the post-pandemic shift back to offices, this represents a missed opportunity. Also, the convenience store segment in strong in many other car-dominated cities across the globe, with many integrating parking space or placed strategically at gas stations, which was rare in Riyadh. Circle K, a major global plater, as a grand total of five locations in the Kingdom. Part of the problem is cultural, as the 50,000 individually operated corner stores across the Kingdom will often leverage cheap migrant labor to take orders from customers as they sit in their vehicles, but big-name players rapidly upgrading in-store experiences could encourage Saudis to get out of their vehicles and possibly spend more.

According to Euromonitor, the segment is recording a healthy 6% annual growth in retail value (albeit from a low base of around USD 1 billion), but this could increase as the fuel retail market is being rapidly consolidated due to legislative changes. For now, gas stations are mostly owned by individuals, but as part of Vision 2030, new licenses are only being granted to companies, which could mean the market gets consolidated into a dozen or so large players over the next few years.

Currently, the convenience store market in Saudi Arabia is predominantly occupied by privately owned or locally listed companies such as Al-Othaim Markets (4001.SE), which interestingly was 21x oversubscribed when it first listed in 2008. A key growth avenue for major convenience store retailers is partnering up with established food delivery services. The major food delivery apps are already expanding into the grocery segment, but with convenience stores the potential for wider coverage and faster delivery times, this could be a significant opportunity.

Widespread use of food delivery apps prompts look into aggressive local acquisitions of European player

The food delivery market is far more mature with expected annual revenues of USD 10 billion for 2023 at a 9.28% CAGR. This format was culturally ingrained long before the rise of apps due to cheap petrol and migrant labour. Food delivery apps and online grocery shopping now occupy a 70% market share in the Kingdom’s food industry. The young tech-savvy locals working at this conference gave me puzzled looks when I asked where to go out for lunch as they seemed to subsist purely on a diet of delivered food (mostly of the fast variety).

Major players in this market are Talabat, Hunger Station (both owned by Germany’s Delivery Hero – DHER.DE), Mrsool (private), and Careem Now (owned by Uber – UBER.N). Delivery Hero appears to be rapidly cornering the market, with an attempted buyout of Mrsool in 2021. Despite that not coming to light, the local player may be at a disadvantage and if app downloads are anything to go by, it is falling out of fashion.

A quick gloss over Delivery Hero’s MENA region, including key territories such as Saudi Arabia, Turkey, Kuwait, and UAE, show that the segment contributes 19% of their anticipated Group GMV of EUR 46 billion, totalling EUR 2.77 billion of revenues (26% of group) in FY23e. This segment is characterized by stable single-digit growth, with margin improvements offsetting declines in other geographical segments, as indicated by their most recent Q323A results. With its shares nearing all-time lows, the Company could be an interesting proxy. However, there are market concerns related to its free cash flow generation and balance sheet given its positive net debt of EUR 3.67 billion. Additionally, Delivery Hero is currently experiencing a downgrade cycle in other regions, which poses challenges to its topline performance. Until the current headwinds subside, it remains a company to keep an eye on. Delivery Hero is expected to incur a net loss of around EUR 712 million in FY23e.

The Saudi Exchange’s tough barriers to entry a reason to look for investment alternatives

Saudi Arabia’s Tadawul Stock Exchange remains largely off-limits to foreign retail investors. The bourse permits only established institutional foreign investors to trade. A qualified foreign investor, for the purposes of the Saudi exchange, must be licensed locally or subject to regulatory oversight and has at least USD 500 million in assets under management.

Retail investors looking to gain access to this market could gain exposure through exchange-traded funds (ETFs) such as iShares MSCI Saudi Arabia ETF (KSA), which tracks 118 Saudi stocks. Although interestingly, LSEG data reported net outflows of over USD 200 million from US equity funds tracking Saudi Arabia this October owing to perceived “regional instability”, with iShares MSCI Saudi Arabia ETF cutting 20% of what was held at the beginning of the month. That said, the ETF has since seen a bounce back from its October-lows.

On the contrary, the Hong Kong Stock Exchange successfully debuted the CSOP Saudi Arabia ETF (2830.HK; 82830.HK), marking Asia’s first ETF tracking the Tadawul. The product is composed of 57 Saudi stock constituents with market capitalization totalling over USD 270 million. HK/China investors can now gain exposure to Saudi Aramco (2222.SE), Saudi National Bank (1180.SE) and Al-Othaim Markets (4001.SE) in HKD/CNY.

The Hong Kong government’s widely-publicised overtures to Saudi Arabia and other Gulf kingdoms seek to enhance investment ties and trade, as the city seeks to avoid reliance on western funds which are more sensitive to the negative press and hostile US policy towards the Special Administrative Region. We also think that the broader enhancement of bilateral relations between Riyadh and Beijing has the potential offset capital flight by Western investors in both markets, who often withdraw funds as a knee-jerk reaction to geopolitical trends without necessarily considering underlying fundamentals as seen of late.

Currently, we hold shares in the CSOP Saudi Arabia ETF (2830.HK; 82830.HK), as means to gain exposure into this emerging market, which we believe will be one of the top performers into 2024.

Disclaimer: This research piece above is for informational, entertainment, educational, and/or study or research purposes only. The information contained herein or discussed does not, should not, and cannot be construed as or relied upon and, for all intents and purposes, does not constitute or provide professional financial, investment, or any other form of advice. This research does not and should not be construed as an offer to sell or the solicitation of an offer to buy any securities or any other financial instruments in any jurisdiction, including where such actions are illegal. This research is not intended for publication in jurisdictions where it would violate laws. The research does not consider individual investment objectives or financial positions and merely expresses the opinions of its authors. Any investment involves taking substantial risks, including (but not limited to) the complete loss of capital. Every investor has different strategies, risk tolerances, and time frames. You are advised to perform your own independent checks, research, or study, and you should consult a licensed professional before making any investment decisions. The assumptions and parameters discussed or used are not the only reasonable ones, and no guarantee is given for their accuracy, completeness, or reasonableness. No promise is made that any indicative performance return will be achieved. The research is derived from public information sourced by Pyramids and Pagodas. No representation or warranty is given for the reliability, completeness, timeliness, accuracy, or fitness of this research, nor is any responsibility or liability accepted for any loss or damage. The authors (Pyramids and Pagodas) shall in no event be held liable to any party for any direct, indirect, punitive, special, incidental, or consequential damages arising directly or indirectly from the use of any of this material.