Plover Bay Technologies (1523.HK) – Another strong year coupled with preparation to split in two

2025 results deliver margin expansion and another year of excess cash returns, but the real headline is its decision for a US spinoff

We first invested in Plover Bay Technologies (1523.HK, “Plover Bay”) in 2017, when its market cap was around USD 142 million, well before we launched our Substack in 2022. Plover Bay has had a formidable run (market cap of USD 1.22 billion today) - manufacturing routers and sells subscriptions for always-on 5G connectivity at a time when IoT and Starlink have taken off.

Since then, we have covered the Company through:

Plover Bay Technologies (1523.HK) – A milestone year with strong growth and expanding opportunities

In that time, Plover Bay has done what it said it would do: grow revenues, expand margins, and hand back the excess. FY25 was no different on the financial front. But the simultaneous announcement of a proposed spinoff of the North American business onto Nasdaq was not something anyone had penciled in.

Or was it? In our FY24 write-up, we noted:

With a majority of its business (64% of revenues) and growth (38% yoy) coming from the US, to us, we think it could be advantageous to do a secondary listing in the US to enhance liquidity, tap into a different shareholder base, as well as increase overall visibility for the business.

Management has gone one step further than a secondary listing; they are proposing full separation. We think the logic is sound, but do execution complexity and economic trade-offs deserve more scrutiny than the market has given them? We’ll look to unpack both the numbers and the strategic pivot.

Another year of profitable, capital-light growth

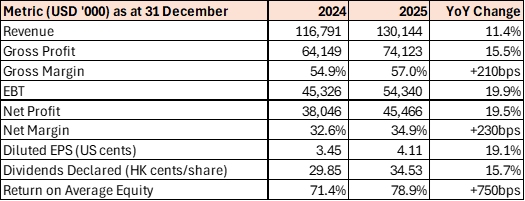

Revenue growth of 11.4% looks modest compared to FY24’s 24% clip, but this number deserves context. Management revealed on the earnings call that tariff-related uncertainty caused Plover Bay to halt US shipments for approximately 1.5 months during Q225. For a Company where North America represents 59% of revenue, that is a material headwind that was entirely self-imposed out of prudence. At a monthly US revenue run rate of roughly USD 6.4 million, the lost revenue from the halt is likely in range of USD 8-10 million. Adding that back implies a normalized revenue growth rate closer to 18-19%, which is fully consistent with the Company’s historical trajectory.

More importantly, profit growth significantly outpaced revenue growth. This is the hallmark of the Plover Bay model: each incremental dollar of revenue carries higher margins because of the growing software and subscription layer sitting on top of the hardware. Net profit margins expanded to nearly 35%, and ROE hit 79%, numbers that would make most enterprise hardware companies envious.

Where the revenue growth is (and isn’t)

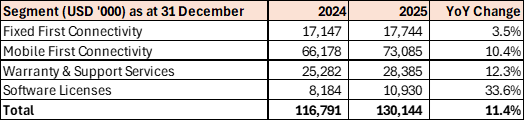

Mobile First Connectivity remains the engine, now representing 56% of total revenue. Starlink-related products contributed to the strong volume growth here, with management noting they now cover Starlink’s entire product line and are developing “companion products”, integrated boxes combining Starlink antennas with 5G routers (like the Peplink Antenna Max S).

The standout is Software Licenses at +33.6%, validating the thesis we have been tracking since our first write-up: that recurring and subscription-based revenue is the real prize. Total recurring revenue reached USD 37.6 million, or 28.9% of total sales, up from 27.6% in FY24. The subscription take-up rate jumped to 38.6% from 34.2%, and devices with active subscriptions increased 25% yoy. The contract liability backlog (essentially prepaid future revenue) stands at USD 38.5 million, up 20% yoy, providing strong forward visibility.

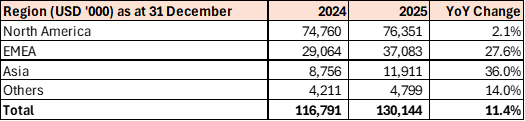

The geographic mix tells the more nuanced story. North America’s 2.1% growth is entirely attributable to the Q2 shipment halt. Had the Company shipped normally, North American growth would likely have been in the low-to-mid double-digits. Meanwhile, EMEA surged 27.6% and Asia jumped 36.0% and these are not small bases anymore. EMEA growth is driven by some hefty contracts: hypermarket chain across 42 locations in France, a major EU infrastructure project where Plover Bay displaced a close competitor, and growing traction in tele-operations for mining equipment.

This geographic diversification is the foundation for the spinoff thesis and, critically, it means the Retained Group (ex-North America) is not the “leftover” entity that some investors might assume. More on this below.

The margin flywheel continues to roll smoothly

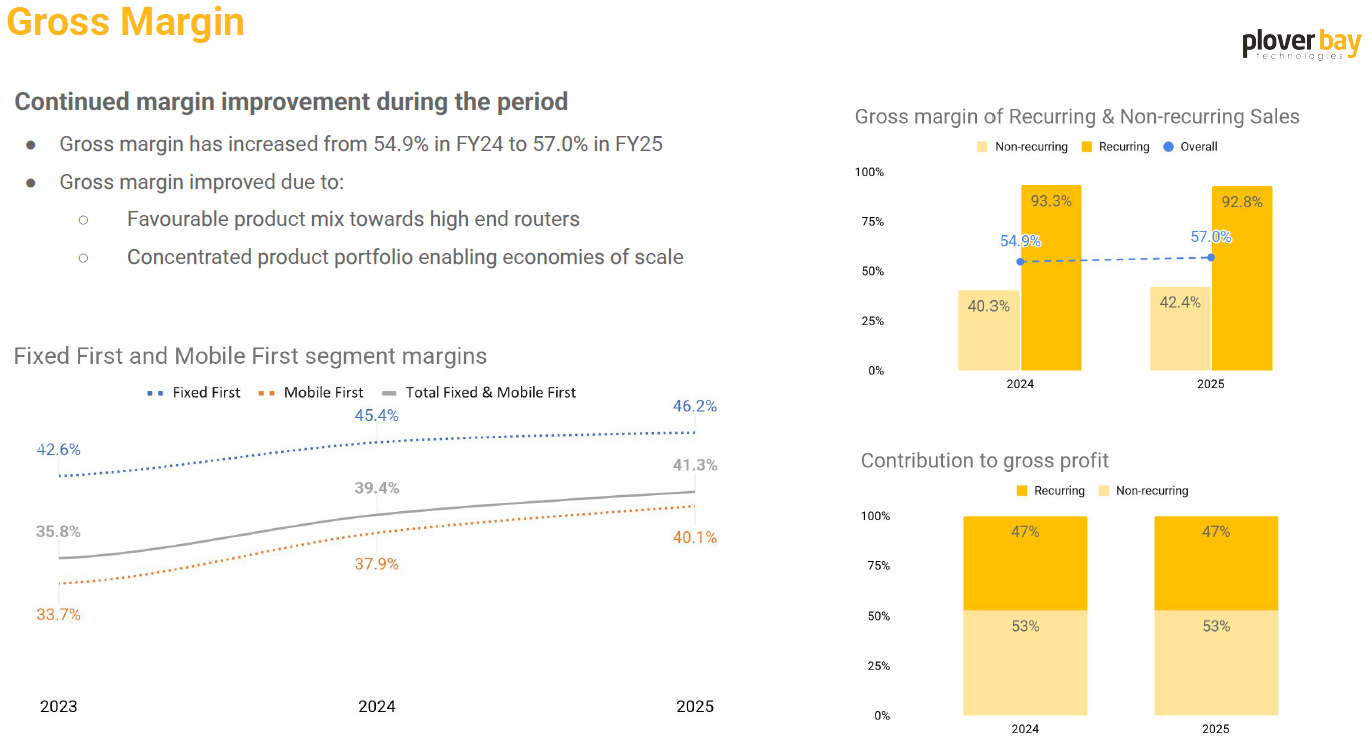

Gross margin expanded 210 basis points to 57.0%, driven by:

Favorable product mix shifting toward higher-end routers

Economies of scale in high-volume models

Recurring revenue at 93% gross margins contributing a larger share

The margin chart from the presentation shows a steady upward progression across its combined hardware margin, while recurring revenue margins remain above 90%. As the subscription layer compounds, this structural margin expansion should continue.

On the cost side, total operating expenses rose to USD 22.1 million from USD 20.6 million, but as a percentage of revenue actually declined from 17.6% to 17.0%. R&D spend increased 18% to USD 10 million (7.7% of revenue), reflecting investment in new products and AI capabilities. Selling expenses actually fell, from USD 4.3 million to USD 3.7 million, demonstrating the efficiency of the channel partner model.

Management was candid on the call about rising component costs, particularly for RAM and storage. However, they deliberately avoided price increases to entry-level products, because these are the gateway to multi-year subscriptions. For high-end models, they indicated the market would accept price increases without issue. This pricing discipline is a classic Plover Bay move: protect the installed base expansion, and monetize through software over time.

Balance sheet is clean as a whistle

The Company fully repaid its bank borrowings during the year, leaving it with USD 67.4 million of gross cash and zero debt. Operating cash flow was USD 52.2 million, comfortably funding the USD 44.3 million in dividends paid during the year.

Total dividends declared for FY25 were USD 49 million against net profit of USD 45.4 million, implying a payout ratio of approximately 108%, which underscores the commitment founder Alex Chan has always articulated: distribute excess cash, reinvest only where it compounds.